Every strategy offsite I've attended in the last five years features the same slide: "Build vs. Buy Analysis." Two columns. Pros and cons. A recommendation that comes down to gut feel dressed up in a framework.

The slide is wrong, because the question itself is broken.

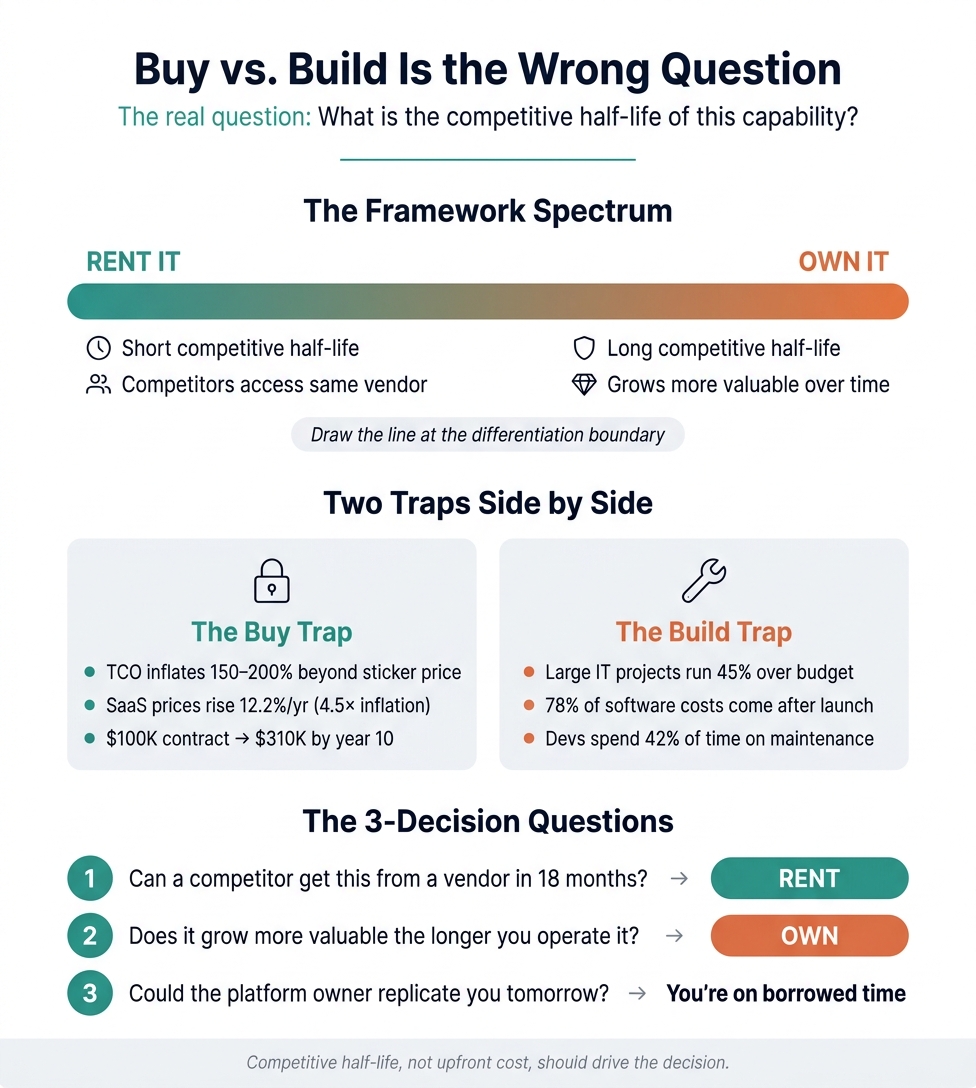

The real question is: what is the competitive half-life of this capability? How long before it becomes table stakes? How long before competitors access the exact same thing from the same vendor?

Short half-life capabilities (FHIR API compliance, basic ambient AI scribes) should be rented. Long half-life capabilities (proprietary clinical datasets, FDA-cleared algorithms) must be owned. Build something about to become commodity and you've volunteered for a permanent maintenance tax on a depreciating asset. Rent something genuinely differentiating and you've handed your advantage to someone else's product roadmap.

The buy trap costs far more than the sticker price. Integration, training, and customization inflate total cost of ownership by 150 to 200%. SaaS price inflation runs at 12.2% annually, 4.5x general inflation. A $100K contract becomes $310K by year ten. Vendors engineer switching costs that make leaving prohibitively expensive.

The build trap is equally punishing. Large IT projects run 45% over budget and deliver 56% less value than predicted. 78% of lifetime software costs accrue after launch. Developers spend 42% of their week on maintenance and technical debt.

The case studies are instructive. Veeva built a $3B business on Salesforce, then walked away in 2022, calling the platform "too risky and too expensive." Building on Salesforce was the right early decision for speed. Staying after differentiation matured was the mistake. Epic, holding 42% of acute care EHR market share, just launched a no-code AI agent builder that directly threatens every digital health startup whose value proposition is "we understand your Epic data."

Own the differentiating layer. Rent the commodity layer. Draw the line precisely at the differentiation boundary.

Tempus AI runs on commodity cloud but owns connections to 65%+ of academic medical centers, 2M+ clinical records, proprietary ML models, and 82 patents. The cloud is interchangeable. The dataset is not. Flatiron built its own oncology EHR rather than building on Epic, giving it direct access to structured data at the point of care. The EHR became the data asset.

For any capability, I ask three questions. Can a competitor get equivalent capability from a vendor within 18 months? If yes, rent it. Does this capability grow more valuable the longer we operate it, through data accumulation, workflow integration, or network effects? If yes, own it. If the platform owner entered this market tomorrow, would we have anything they couldn't replicate? If no, you are building on borrowed time.

Renting for speed early, then transitioning to ownership as differentiation matures, is a legitimate strategy. But only if you plan the exit before you sign the contract.

The competitive half-life of software: a framework for build-vs-buy

Build-vs-buy is a false binary because it ignores time. The real question is: what is the competitive half-life of this capability — how long before it becomes table stakes? Capabilities with short half-lives (ambient AI scribing, FHIR compliance, basic analytics) should be rented. Capabilities with long half-lives (proprietary clinical data, FDA-cleared algorithms, deep workflow integration) must be owned — or competitors accessing the same commodity tools will erase your advantage. The companies that win — Tempus, Flatiron Health, Veracyte — correctly identify where differentiation lives, own that layer, and rent everything else. The companies that lose build their core IP on someone else's product roadmap, then get squeezed when the platform owner notices their market.

Both paths fail — just in different ways

The data is brutal on both sides of the build-vs-buy ledger, which is precisely why the binary framing misleads.

The "buy" trap is more expensive than it appears. Gartner's 2025 SaaS Economics analysis found that hidden integration, training, and customization costs inflate SaaS TCO by 150–200% beyond the sticker price. Organizations routinely overlook 50–70% of total costs when calculating software ownership expenses. SaaS inflation compounds the problem: the Vertice SaaS Inflation Index (2026) pegs SaaS price inflation at 12.2% annually — 4.5× general inflation — sustained for three consecutive years. Per-employee SaaS costs hit $9,100 by end of 2025, up from $7,900 in 2023. Meanwhile, Zylo's 2025 SaaS Management Index reports that 66.5% of IT leaders experienced unexpected charges from consumption-based or AI pricing models, and the average enterprise wastes $18 million annually in unused SaaS licenses.

The "build" trap is equally punishing. The McKinsey–Oxford study of 5,400 large IT projects found they run 45% over budget and deliver 56% less value than predicted. Standish Group's CHAOS 2020 data shows only 31% of projects succeed on time, budget, and scope — 19% fail outright. Forrester's Total Economic Impact model reveals 78% of lifetime software costs accrue after launch, not during initial development. In healthcare specifically, IT projects fail at rates approaching 70% when accounting for delays, overruns, and goal shortfalls.

The resolution isn't to pick the lesser evil. It's to recognize that each path is optimal for a different class of capability — determined by competitive half-life.

When vendors become predators: healthtech case studies

The most instructive examples come from healthcare and life sciences, where platform dependency has produced spectacular squeezes.

Veeva Systems and Salesforce is the definitive healthtech platform-risk case study. Veeva built a $3 billion+ revenue business on Salesforce's platform over 15 years, serving as the dominant CRM for life sciences. In December 2022, Veeva announced it would not renew the Salesforce partnership (expiring September 2025) and would migrate its entire CRM to its proprietary Vault Platform. CEO Peter Gassner called Salesforce "too risky and too expensive." The reasons: declining customer experience from outages on both Salesforce and AWS infrastructure, constraints on product roadmap tied to Salesforce release cycles, and the existential risk that Salesforce would enter Veeva's market — which it did, launching Salesforce Life Sciences Cloud at $350/user/month. Every pharma company using Veeva CRM now faces a forced migration costing $1.5–4 million per implementation with 6–24 month timelines. The lesson is nuanced: building on Salesforce was the right early decision for speed-to-market. Staying after differentiation matured was the mistake.

Epic's Agent Factory (announced HIMSS26, March 2026) represents the newest and most aggressive example of a platform owner absorbing an entire ecosystem's value. Epic — which holds 42.3% of acute care EHR market share (54.9% by bed count) — launched a no-code AI agent builder alongside proprietary clinical AI (Art), patient chatbot (Emmie), revenue cycle AI (Penny), and clinical trials management (Forward). This directly threatens every digital health startup whose value proposition amounts to "we know what your Epic data means and can do something useful with it." Epic earlier gutted its App Orchard marketplace and replaced it with the more restrictive Vendor Services program. Integration projects consistently take 6–18 months and often exceed budget — one CTO reported $300,000 in labor over 8 months. A 2023 KLAS report found 68% of health systems struggle with Epic interoperability.

Oracle's acquisition of Cerner for $28.3 billion (June 2022) devastated an ecosystem of partners who built on Cerner's APIs and data models. Oracle cut Cerner's workforce by ~50%, lost 57 unique acute care customers in three years, and saw market share decline from 25% to 22.9%. A five-day outage in April 2025 affected 45 of Community Health Systems' 71 hospitals. Oracle's strategy prioritized Oracle Cloud Infrastructure integration, deepening vendor lock-in while degrading the partner ecosystem.

AWS entering healthcare follows the same playbook as AWS in every other vertical. From Amazon Comprehend Medical (2018) to HealthLake (2021) to HealthOmics (2022) to Amazon Connect Health (March 2026, $99/user/month), Amazon has systematically built competing products while hosting the startups it competes with. Your infrastructure provider sees which use cases are growing and which markets are profitable enough to enter.

Outside healthtech, VMware/Broadcom provides the most extreme vendor-squeeze case: post-acquisition price increases of 800–1,500%, elimination of perpetual licenses, consolidation of ~8,000 SKUs into two bundles, and 72-core minimums. AT&T and United Healthcare have sued. The EU Cloud Providers consortium (CISPE) formally complained. And Twitter/X destroyed an entire startup ecosystem overnight in February 2023, raising API costs from $2,899/month (Premium) to a $42,000/month Enterprise minimum — a pattern where "platforms embrace developers until those developers become competitive threats."

The maintenance tax nobody budgets for

The case against building everything is equally damning, grounded in data that companies systematically ignore.

Stripe's Developer Coefficient study (Harris Poll, 2,000+ respondents) found developers spend 42% of their work week — 17.3 hours out of 41.1 — on maintenance and technical debt. That breaks down to 13.5 hours on technical debt maintenance and 3.8 hours fixing bad code. The global opportunity cost: roughly $300 billion in GDP lost annually from developer inefficiency. The Consortium for Information & Software Quality (CISQ, co-founded by Carnegie Mellon SEI) estimates accumulated US technical debt at $1.52 trillion as of 2022.

McKinsey's research shows 30% of CIOs believe more than 20% of their technical budget — nominally earmarked for new products — gets diverted to resolving tech debt. Organizations with high technical debt spend 40% more on maintenance and ship new features 25–50% slower than competitors. Gartner's widely cited figure holds that companies spend an average of 70% of IT budgets on "run the business" maintenance, leaving less than 30% for innovation. Forrester's survey of 3,700+ companies corroborates this at 72%.

In regulated industries, the burden compounds. Every custom software change in life sciences requires re-validation documentation, audit trail maintenance, and compliance testing — costs that are ongoing and mandatory, not discretionary. Traditional Computer System Validation (CSV) in life sciences involves blanket testing without risk prioritization. Commercial validated platforms (Veeva Vault, MasterControl, Qualio) shift this burden to the vendor; custom builds absorb it entirely. HIPAA and FDA compliance add $20,000–$50,000+ to custom EHR development costs, with hidden compliance costs adding 10–18% to overall project cost.

The implication is clear: building commodity capabilities means volunteering for a permanent maintenance tax that compounds annually, while the competitive value of that capability simultaneously erodes as vendors commoditize it.

Five frameworks that predict where differentiation lives

The "competitive half-life" concept draws on several established strategic frameworks, all converging on the same insight.

Simon Wardley's Mapping (2005–present) plots every technology component along an evolution axis from Genesis → Custom Built → Product → Commodity. Components on the left have long competitive half-lives; components on the right approach zero. Wardley notes computing took ~40 years to move from Genesis to Commodity. In the AI era, this cycle compresses dramatically. The strategic prescription: build what's in Genesis/Custom; rent what's in Product/Commodity.

Geoffrey Moore's Core vs. Context (Dealing with Darwin, 2005) introduces the Competitive Advantage Period (CAP) — essentially competitive half-life by another name. Core activities create sustainable differentiation. Context activities are necessary but not differentiating. Moore's framework produces a powerful decision rule: "Markets reward core initiatives but never context initiatives. The market only responds to context by punishing businesses if context is implemented badly." Build core; buy context.

Gartner's Pace-Layered Application Strategy maps directly onto half-life thinking. Systems of Innovation have the shortest competitive half-life (months). Systems of Record have effectively infinite half-life (already table stakes). Systems of Differentiation sit in between (years). Buy or rent Systems of Record, build Systems of Innovation, and partner on Systems of Differentiation until they prove themselves.

Clayton Christensen's Law of Conservation of Attractive Profits (The Innovator's Solution, 2003) predicts that when modularity and commoditization destroy profits at one layer, proprietary opportunities emerge at adjacent layers. IBM outsourced chips and OS — Intel and Microsoft captured all the profits. This is why building commodity capabilities is a strategic error: the profits will migrate elsewhere.

The Technology S-Curve (Richard Foster, 1986) provides the timing mechanism. Competitive half-life is longest during the acceleration phase and shortest at the plateau. When competitors can't replicate you because the technology is still being figured out, your advantage persists. Once you're on the plateau, everyone converges and the advantage evaporates.

Companies that got the layering right

The winners share a common architecture: own the differentiating layer, rent the commodity layer.

Tempus AI (IPO'd June 2024, $6.1 billion valuation, ~$952 million revenue) runs on commodity cloud infrastructure but owns the differentiating elements: connections to 65%+ of academic medical centers, 2 million+ clinical records, proprietary ML models for treatment matching and drug target identification, CLIA-certified sequencing labs generating new molecular data daily, and 82 issued US patents plus 136 pending. The cloud is interchangeable; the structured clinical-molecular dataset is not. Tempus was the first NGS lab to integrate with Epic (200+ integrations), creating a data flywheel where diagnostics generate data that feeds the AI that improves diagnostics.

Flatiron Health (acquired by Roche, 2018, ~$1.9 billion) made the critical decision to build its own specialized oncology EHR (OncoEMR) rather than building on Epic or Cerner. This gave Flatiron direct access to structured oncology data at the point of care — the most valuable data capture point in the value chain. The EHR itself became the data asset, connecting 4,200+ providers at 800+ cancer care locations. Flatiron became the platform others integrate with, not the reverse.

Veracyte (founded 2008) built proprietary genomic diagnostic tests using RNA whole-transcriptome sequencing and ML classifiers — then acquired the NanoString nCounter diagnostics platform to own the instrument layer, avoiding dependency on third-party lab infrastructure for global distribution. They also acquired Decipher Biosciences for $600 million (adding 85,000+ annotated urologic cancer samples) and C2i Genomics for $70 million (whole-genome MRD capabilities). Veracyte's differentiation lives in algorithms, data, and clinical evidence — not in instruments or cloud infrastructure. The result: ~40% US market share in thyroid testing, ~70% in prostate genomic testing, and 10 consecutive quarters of 20%+ revenue growth.

Major pharma companies exhibit the same pattern. Novartis built proprietary "AE Brain" algorithms on commodity AWS infrastructure for adverse event monitoring. Merck deployed its Real World Data Exchange on AWS — the cloud is rented, the data relationships are owned. The consistent insight: cloud computing and basic NLP are commodity layers to rent; clinical data relationships, regulatory expertise, and therapeutic algorithms are differentiation to own.

A half-life map for healthtech capabilities

The frameworks above, combined with current market data, produce a practical competitive half-life spectrum for healthcare technology:

| Capability | Half-life | Evidence | Strategy |

|---|

| FHIR API compliance | Near-zero | CMS/ONC mandated standard; multiple vendors offer it | Rent |

| Basic ambient AI scribe | 6–18 months | Menlo Ventures: 67% of providers likely to switch vendors within 3 years; "customers view scribing as becoming commoditized" | Rent |

| Telehealth platform | Short | Fully commoditized post-COVID | Buy off-the-shelf |

| Patient engagement tools | Short–medium | Rapidly copied; low switching costs | Rent or buy |

| EHR system | Very long | Massive switching costs; few viable vendors | Buy (limited options) |

| Domain-specific AI workflows | Medium–long | Integration depth creates switching costs | Build |

| FDA-cleared clinical AI | Long | Regulatory + data moat; peer-reviewed validation | Build |

| Longitudinal clinical data platform | Very long | Unique data asset; network effects; irreplaceable | Build |

The key accelerators of commoditization are: open-source alternatives emerging (Llama vs. GPT-4), platform incumbents absorbing the feature (Epic adding AI scribe), regulatory mandates standardizing it (21st Century Cures Act), low switching costs, and multiple well-funded competitors racing on the same capability. The key decelerators are: proprietary data moats, regulatory barriers (FDA clearance), network effects, deep workflow integration, and domain expertise embedded in the product.

Bessemer Venture Partners' 2026 State of Health AI report confirms: "Access to longitudinal clinical data is likely to emerge as a core competitive advantage." Revenue durability in health AI requires "ROI so clear customers will pay 2–3× more than commodity alternatives." McKinsey adds that the top 10 US health systems control ~175,000 beds and massive data assets — making clinical data partnerships an increasingly scarce and valuable resource.

SaaS vendor economics are tilting the calculus toward owning more

Several compounding trends make the "rent everything" strategy increasingly dangerous.

Price escalation is structural, not cyclical. SaaS inflation has run at 11–12% annually for three consecutive years against ~2.7% general inflation. Standard contractual escalation clauses run 4–7% annually, but major vendors are rewriting renewal protections: Microsoft, Salesforce, and ServiceNow now use compounding per-year rate caps rather than one-time uplifts, dramatically changing long-term economics. At the industry-average 12% annual escalation, a $100,000 SaaS contract becomes $310,000 by year 10 — a 210% cumulative increase.

Consolidation amplifies pricing power. Private equity SaaS acquisitions grew 28% in 2024, with PE-owned vendors imposing price increases as high as 900%. The Broadcom/VMware case — 800–1,500% increases post-acquisition — is extreme but directional. Salesforce now derives ~72% of go-forward ARR growth from price increases rather than new customer acquisition. Adobe raised Creative Cloud prices 16.7–50% while rebranding tiers. Docker increased pricing 67–80%.

"SaaS shrinkflation" reduces value at stable or higher prices. CFO Dive reports 28% of SaaS contracts experienced shrinkflation in 2024 — reduced features or tiers at the same or higher price point. Microsoft eliminated lower-tier M365 plans, forcing customers to higher SKUs. Google bundled Gemini AI into all tiers, charging for AI whether customers use it or not. Salesforce added consumption charges on previously unlimited features.

Switching costs are deliberately engineered to compound. Enterprises with 10+ Salesforce integrations show 40% lower churn rates than those with minimal integrations. Organizations with 80%+ Slack adoption show 62% lower switching likelihood. Gartner found that 58% of customers who feel "trapped" eventually leave — but only after absorbing enormous transition costs. The economic moat isn't the product; it's the switching cost.

Conclusion

The build-vs-buy question misfires because it treats all software capabilities as equivalent. They are not. Each capability has a competitive half-life — the time before it becomes table stakes — and that half-life determines the correct strategy. Rent capabilities with short half-lives (commodity infrastructure, standardized compliance, commoditizing AI features) because building them means volunteering for a permanent maintenance tax on a depreciating asset. Own capabilities with long half-lives (proprietary data, validated algorithms, deep clinical workflows) because renting them means building your differentiation on someone else's product roadmap — and platform owners inevitably notice profitable markets.

The most dangerous position is the middle: building differentiation on top of a vendor's differentiating layer, as Veeva did with Salesforce or digital health startups did with Epic. The smartest companies — Tempus, Flatiron, Veracyte — draw the ownership line precisely at the differentiation boundary. The Veeva story adds a critical nuance: when to own can matter as much as what to own. Renting for speed early, then migrating to ownership as differentiation matures, is a legitimate strategy — provided you architect for the transition from day one. In a world where SaaS inflation runs at 4.5× general inflation and AI capabilities commoditize in months rather than years, getting the half-life assessment right is not just a technology decision. It is the strategy.

Commissioned from our research desk. Subject to final editorial discretion.