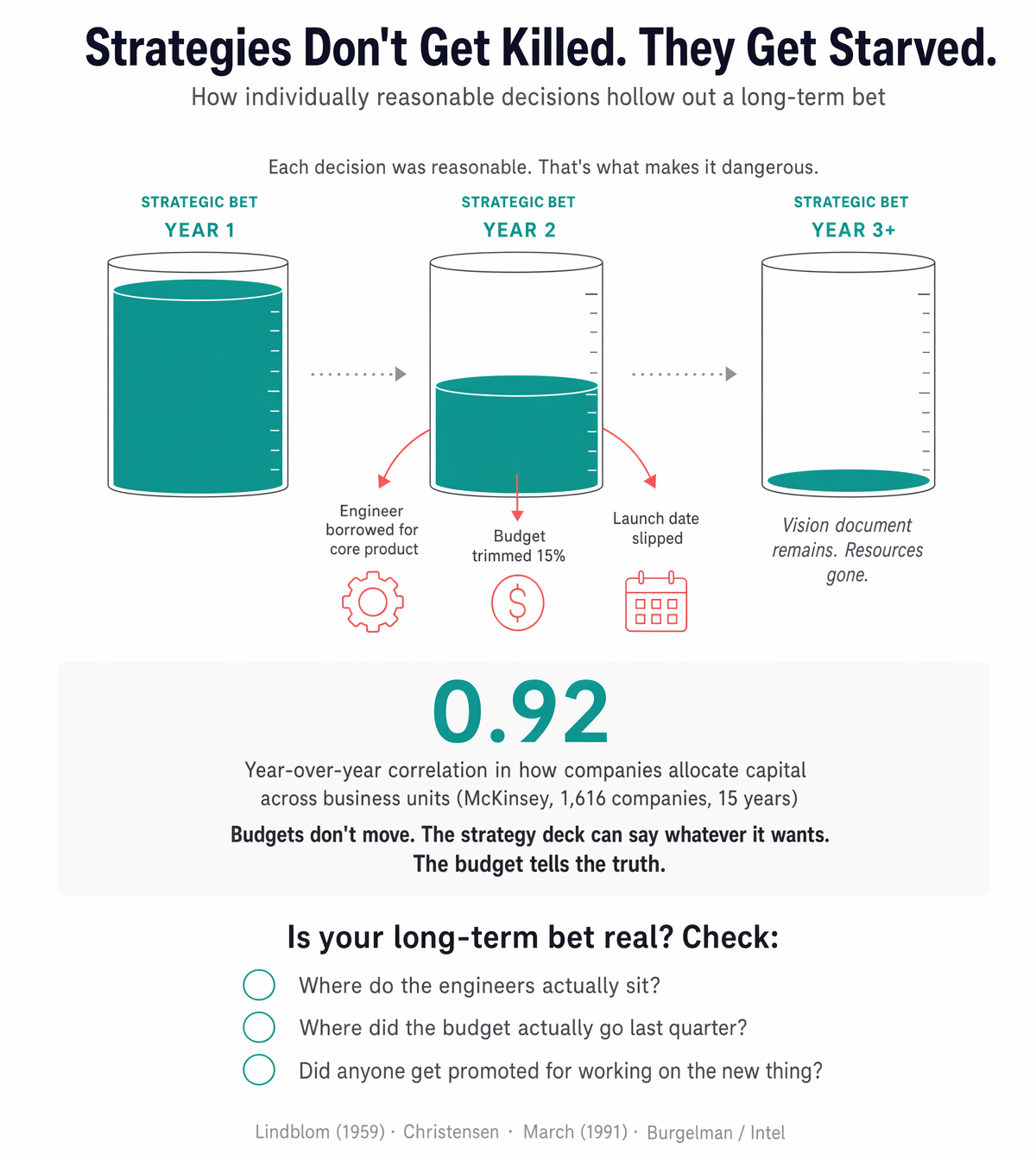

Nobody satisfies a long-term strategy to death. They starve it. So gradually that no one can point to the moment it happened.

A company makes a bold bet. New platform, new market, new capability. The executive team is aligned. There's a roadmap, maybe even a dedicated team.

Then the quarterly review arrives. The core business borrows an engineer from the new initiative. Just one, just for six weeks. The launch date slips, so marketing spend gets pushed. A key hire is deferred. The pilot narrows from three markets to one.

Every single one of these decisions is reasonable. Every single one can be defended in a meeting. The person making each call is being responsible. And that's exactly the problem.

Christensen put it simply: strategy is determined by what comes out of the resource allocation process, not by the intentions that go into it. The core business wins every micro-decision because it has revenue, dashboards, and quarterly targets. The future business has a PowerPoint deck.

McKinsey studied 1,616 companies over 15 years and found capital allocation across business units correlates at 0.92 year-over-year. A third of companies reallocate just 1% of capital annually. The strategy deck changes. The budget doesn't. Top-third reallocators earned 30% higher annual returns.

Gerry Johnson called this strategic drift. The dangerous part: small adjustments produce short-term improvements that make the drift harder to detect.

The case studies share a common structure. Kodak's Steve Sasson built the first digital camera in 1975. For two decades, digital projects were subordinated to film, priced to protect film margins. Every budget cycle, film looked better on the spreadsheet. Kodak filed for bankruptcy in 2012. No one decided to abandon digital. They just never fully committed.

At Nokia, engineers warned Symbian couldn't compete with iOS. Resources split across five platforms. None ever received enough investment to succeed. Market share went from 49.4% to 3% in six years.

James March's work on exploration vs. exploitation explains why. Exploitation yields returns that are certain and measurable. Exploration yields returns that are uncertain and diffuse. In any budget cycle, exploitation wins.

So what do you do? Awareness alone doesn't fix it. You need structural countermeasures. Ring-fence the budget for the long-term bet and make raiding it visibly costly. Track not just whether the initiative exists, but whether its scope, resources, and timeline have quietly narrowed. Create a dashboard showing the delta between what was originally committed and what's actually flowing.

Most importantly, name the pattern when you see it. Because most strategies don't get killed. They get starved. And nobody notices, because no single decision looks like the one that did it.

How individually reasonable decisions hollow out strategic bets: a research briefing

The academic and practitioner literature provides a remarkably convergent answer to how long-term strategies die. Strategies are almost never explicitly cancelled — they are starved through accumulated micro-decisions, each defensible in isolation, that gradually redirect resources, attention, and talent back toward the core business. This pattern has been independently identified by Charles Lindblom in public policy, Gerry Johnson in strategic management, Clayton Christensen in innovation theory, Robert Burgelman in organizational ecology, and McKinsey in empirical resource allocation research. The quantitative evidence is stark: companies deliver only 63% of the financial performance their strategies promise, [1][2] budgets correlate at 0.92 year-over-year regardless of strategic change, and only 5% of employees can articulate their company's strategy at all. [1][3]

1. Lindblom's "muddling through" and the intellectual origins of incrementalism

Core Paper: Charles E. Lindblom, "The Science of 'Muddling Through,'" Public Administration Review 19(2): 79–88 (Spring 1959).

Lindblom contrasted two models of decision-making. The "rational-comprehensive" (Root) method requires decision-makers to rank all values, identify all alternatives, and choose the optimal solution — a process he argued is impossible for complex problems. The "successive limited comparisons" (Branch) method — his term for how policy is actually made — starts from the status quo and considers only policies that differ marginally from existing ones. [4] Means and ends are intertwined, analysis is restricted to a few nearby alternatives, and agreement among stakeholders substitutes for abstract optimization. [5]

Key quotes from the original paper:

- "No one can practice the rational-comprehensive method for really complex problems." [6]

- Each policy decision should ideally be "only one step... that if successful can quickly be followed by another." [6]

- Lindblom defended incrementalism as "superior to any other decision-making method available for complex problems in many circumstances, certainly superior to a futile attempt at superhuman comprehensiveness." [7]

The 1979 follow-up: In "Still Muddling, Not Yet Through" (Public Administration Review 39(6): 517–526), Lindblom refined the concept into "disjointed incrementalism" — a mutually supporting set of simplifying and focusing stratagems. [8] He distinguished incremental analysis (the method) from incremental politics (the size of changes) from partisan mutual adjustment (the negotiation process). [9] He also introduced "strategic analysis" — any calculated set of stratagems to simplify complex problems. [10]

Critical academic responses:

- Amitai Etzioni's "mixed scanning" (1967): Proposed a middle path — broad scanning to identify general direction, detailed examination of the most promising alternatives. [11] Etzioni argued incrementalism "neglects basic societal innovations" and has a conservative slant. [12]

- Yehezkel Dror (1964): Argued incrementalism is fine for normal times but "a recipe for disaster" when facing crises requiring bold action. [11]

- The "Beagle fallacy": Like a hound with excellent smell but limited sight, incrementalism may cause organizations to miss what appears from unexpected directions. [13]

- Punctuated equilibrium (Baumgartner & Jones, mid-1990s): Long periods of incrementalism are punctured by sudden, dramatic shifts [13] — the dominant model now in policy studies.

- Path dependency challenge: Critics note Lindblom assumed incremental decisions can be reversed, but path dependency theory shows they create lock-in effects that make reversal increasingly difficult. [14]

The bridge to corporate strategy — James Brian Quinn's "logical incrementalism" (1978/1980): Quinn applied Lindblom to corporate strategy, finding that executives "probe the future, experiment, and learn from a series of partial commitments rather than through global formulation of total strategies." [15][16] His critical caveat: "The major weakness of the approach is that it does not guarantee that the various loosely linked decisions will add up to fulfillment of corporate purposes." [17] This is the hinge point connecting Lindblom's descriptive theory to the prescriptive warning about strategic failure.

Henry Mintzberg's emergent strategy (1985): Mintzberg and Waters found that only 10–30% of planned strategies are ever fully realized. [18] Realized strategy is typically a blend of deliberate intent and emergent patterns [18] — a finding that reinforces how accumulated small decisions can overwhelm formal strategic direction.

Sources: Public Administration Review (1959, 1979); Etzioni, PAR 27(5): 385–92 (1967); Quinn, Sloan Management Review, Fall 1978; Mintzberg & Waters, Strategic Management Journal 6(3): 257–272 (1985); Pal, "Lindblom's Lament," Policy and Society 30(1): 9–18, 2011.

2. Strategic drift: Gerry Johnson's framework for how incrementalism becomes maladaptive

Foundational paper: Gerry Johnson, "Rethinking Incrementalism," Strategic Management Journal 9: 75–91 (1988).

Johnson explicitly engaged with Lindblom and Quinn, then reframed incrementalism within organizational culture theory. [19] His central concept: strategic drift is the tendency to develop strategies incrementally on the basis of historical and cultural influences, while failing to keep pace with a changing environment. [20] Sammut-Bonnici (2014) later codified it as "a gradual deterioration of competitive action that results in the failure of an organization to acknowledge and respond to changes in the business environment." [21][22]

Johnson's four phases of strategic drift:

- Incremental change: The organization makes small adjustments and remains roughly aligned with its environment. No cause for alarm. [23][22]

- Strategic drift: The external environment accelerates in change, but the organization continues operating as before. [22][23] Short-term improvements mask the widening gap. Johnson noted: "This pattern of drift is made more difficult to detect and reverse, because changes may achieve some short-term improvement in performance, thus tending to legitimise the action taken." [24]

- Flux: The gap becomes undeniable. Indecision is common. [25] The organization lacks clear direction. [26]

- Transformational change or death: Either radical transformation occurs, or the organization fails. [23][22]

The organizational paradigm as the mechanism: Johnson defined this as "the set of beliefs and assumptions, held relatively common through the organization, taken for granted... which plays a central role in the interpretation of environmental stimuli and configuration of organizationally relevant strategic responses." Both intended and realized strategy are configured within the paradigm's parameters [27] — meaning decision-makers literally cannot perceive the need for change through their existing cognitive framework. This explains why each incremental decision seems rational from inside the organization while being collectively maladaptive.

Causes Johnson identified: organizational inertia, cognitive mapping that limits perception, culture that frames all decisions, homogeneous mindsets at leadership levels, [28] preservation of the status quo, and marketing myopia (Levitt's concept). [21]

Sources: Johnson, SMJ 9: 75–91 (1988); Sammut-Bonnici, Wiley Encyclopedia of Management (2014); Johnson, Scholes & Whittington, Exploring Corporate Strategy (multiple editions).

3. The mechanism of strategic starvation: Christensen, Burgelman, and the resource allocation literature

Christensen's resource allocation insight

Clayton Christensen's most underappreciated contribution from The Innovator's Dilemma (1997) and The Innovator's Solution (2003) isn't the concept of disruption — it's his analysis of how internal resource allocation processes systematically kill strategic bets. His central claim: "Strategy is determined by what comes out of the resource allocation process, not by the intentions and proposals that go into it." [29]

The mechanism: most innovation proposals originate deep within the organization, not from the top. [30] Middle managers play the critical filtering role, and their careers depend on sponsoring winning projects. [30] Projects targeting current customers with known markets always win the resource allocation competition over proposals with uncertain markets. [31] As Christensen put it: "The filters in the resource allocation process of successful companies become so well attuned to the successful strategy that they filter out all but the initiatives that sustain the existing business." [32][33]

The asymmetry is structural. The core business has revenue, customers, dashboards, quarterly targets, proven margins, and powerful internal advocates. The future business has a vision document, uncertainty, unproven markets, and no established political constituency. Every micro-decision favors the present over the future because the present is legible and the future is not.

Christensen's RPV framework (Resources, Processes, Values) explains why: as companies mature, capabilities shift from residing in people to being embedded in processes and values. [34][35] These become invisible filters that systematically starve projects that don't fit the existing business model.

Andy Grove, quoted by Christensen: "To understand a company's strategy, look at what they actually do rather than what they say they will do." [36]

Burgelman's intraorganizational ecology

Robert Burgelman at Stanford developed an ecological model of strategy-making. In "Intraorganizational Ecology of Strategy Making and Organizational Adaptation" (Organization Science, 1991), he argued that internal selection pressures determine which strategic initiatives survive and which die, analogous to natural selection. He distinguished between induced strategic behavior (aligned with existing strategy; thrives because it fits the current structural context) and autonomous strategic behavior (new opportunities recognized by individuals; kept "under the radar" by middle managers who must hide and protect early ideas before they're strong enough to survive internal ecological selection). [37]

The Intel DRAM case is the paradigmatic illustration. In "Fading Memories" (Administrative Science Quarterly, 1994), Burgelman showed that Intel's middle managers, through their individual resource allocation decisions on the factory floor, gradually shifted manufacturing capacity from DRAM to microprocessors based on margin calculations — long before top management officially decided to exit DRAM. [38] The strategy changed at the operational level through accumulated micro-decisions before the official strategy was updated. A middle manager said exiting DRAM was "tantamount to Ford deciding to exit the car business" [39] — yet it happened without a formal decision.

In Strategy Is Destiny (2002), Burgelman documented how Intel's successful focus on PC processors created "coevolutionary lock-in" — the strategy-making process became increasingly tied to the PC market segment, [40] and the very success of focus created inertia that made it harder to pursue autonomous strategic initiatives in new domains.

The Bower-Burgelman process model

Joseph Bower (Harvard, 1970) and Burgelman together established that a company's realized strategy emerges not from formal statements of corporate strategy, but from the pattern of resource commitments that originate across every level of the firm. Their edited volume From Resource Allocation to Strategy (Oxford UP, 2005) is the definitive academic compilation, bringing together Bower, Burgelman, Christensen, and Sull, [41] with chapters including "When the Bottom-up Resource Allocation Process Fails" and "No Exit: The Failure of Bottom-up Strategic Processes."

Don Sull's "active inertia"

In "Why Good Companies Go Bad" (Harvard Business Review, July–August 1999), Donald Sull [42] defined active inertia as "management's tendency to respond to the most disruptive changes by accelerating activities that succeeded in the past." [43] His four hallmarks: strategic frames become blinders, processes harden into routines, relationships become shackles, and values turn into dogmas. [44] The key metaphor: "Organizations trapped in active inertia resemble a car with its back wheels stuck in a rut. Managers step on the gas. Rather than escape the rut, they only dig themselves in deeper." [45] The Economist named active inertia one of the ideas that shaped business management over the past century. [46]

Sources: Christensen, The Innovator's Dilemma (1997); Christensen & Raynor, The Innovator's Solution (2003); Burgelman, Organization Science 2: 239–262 (1991); Burgelman, ASQ 39(1): 24–56 (1994); Burgelman, Strategy Is Destiny (2002); Bower & Gilbert, eds., From Resource Allocation to Strategy (2005); Sull, HBR July–August 1999.

4. Case studies: strategies that died without being killed

Microsoft's mobile strategy

Microsoft had 15% smartphone market share in 2006–2008 with Windows Mobile. [47] After the iPhone launched, each subsequent decision was individually defensible but collectively fatal. Building Zune instead of a smartphone ("iPod was the immediate competitor"). Launching Windows Phone 7 as a full reboot in 2010, already three years behind. Acquiring Nokia's phone business for $7.2 billion in 2013 (Satya Nadella internally voted no, arguing Microsoft was "chasing competitors' taillights"). [48] The incremental retreat: 18,000 jobs cut in July 2014 (12,500 former Nokia employees). Nadella releasing Office and Outlook on iOS and Android ("reach more users") — undermining any reason to buy a Windows Phone. [49] A $7.6 billion write-off in July 2015, more than the acquisition price. [50] Selling Nokia's feature phone business for $350 million in 2016. [51] Joe Belfiore confirming in October 2017 that Microsoft was no longer developing mobile features. Each narrowing — fewer phone models, reduced marketing, reassigned engineers — was operationally rational. No single meeting decided to abandon mobile. Bill Gates later called it "the greatest mistake ever."

Kodak engineer Steve Sasson invented the digital camera in 1975. Management's response: "That's cute, but don't tell anyone about it." Over two decades, the pattern repeated: digital initiatives were structurally subordinated to the film division. Digital cameras were deliberately priced to protect film sales. No independent digital department was created — digital projects were embedded within a film-centric organization where middle managers couldn't "think digitally." Each quarterly budget review reinforced investing in film because it showed higher margins than the "still unproven" digital efforts. The company invested $5.1 billion in the Sterling Drug acquisition (1988), draining capital from digital transition. A longitudinal NYU Stern study found that "it was not digital imaging that led to Kodak's downfall — the company failed because key decisions made in the late 1980s and early 1990s limited the company's ability to become successful in businesses beyond imaging." Engineers knew "most photographs would be taken on telephones" but the insight "rarely translated into decisive business action." Kodak filed for bankruptcy in 2012. [22][52]

At 49.4% global smartphone market share in 2007, Nokia recognized the need to shift from hardware to platform competition. [53] But by 2009, Nokia used 57 different and incompatible versions of Symbian. Resources were split across Symbian, Maemo, MeeGo, Meltemi, and eventually Windows Phone — ensuring no single platform received sufficient investment. INSEAD research revealed a fear-driven internal culture: middle managers overpromised and underdelivered on platform readiness because "you can get resources by promising something earlier, or promising a lot." Engineers warning Symbian couldn't compete with iOS were sidelined. The result was what researchers called "pluralistic silence" — no one spoke up about Symbian's limitations. When CEO Stephen Elop declared Symbian obsolete in his "burning platform" memo (February 2011), it killed demand for existing Nokia phones overnight while Windows Phone devices were months from launch. Market share collapsed from 49.4% to 3% by 2013. Microsoft acquired Nokia's handset division [54] for €5.44 billion — roughly what Nokia had spent on Symbian R&D in the preceding five years.

IBM Watson: from "moon shot" to sold for parts

After Watson's Jeopardy! victory in 2011, IBM positioned it as a transformative enterprise AI platform. [55][56] CEO Virginia Rometty called Watson Health a "moon shot" [57] targeting $10 billion in annual revenue. IBM spent over $4 billion in acquisitions (Truven Health Analytics, Merge Healthcare, Explorys, Phytel). [58][59] The incremental hollowing: acquired companies were forced to abandon modern tech stacks for IBM's legacy infrastructure ("Blue Washing") — individually justified as "enterprise consistency" but degrading product quality. [59] Watson for Oncology was deployed using U.S.-centric treatment recommendations inconsistent with local practices in India and China. [55] David Ferrucci, Watson's architect, warned executives the system was designed to "identify word patterns and predict correct answers to questions," not serve as "an all-purpose answer box." [60] The MD Anderson Cancer Center partnership failed after $65 million when Watson provided unsafe treatment recommendations. By 2018, more than a dozen partners stopped or scaled back projects. [61] In January 2022, IBM sold Watson Health to Francisco Partners for approximately $1 billion — a fraction of what was invested. [58][59] IBM launched "watsonx" in May 2023, a completely new AI platform bearing almost no resemblance to the original Watson. [60]

Other examples in brief

Intel's mobile chips: CEO Paul Otellini passed on making chips for the original iPhone in 2006, [62] then sold Intel's ARM-based XScale business for $600 million to "focus on Atom." [63] By the time Intel launched its first phone-ready Atom SoC in 2012, it was five years behind. [64] In 2014, Intel shipped 46 million tablet Atom chips using massive subsidies at enormous losses. [65] In April 2016, Intel cancelled smartphone Atom chips entirely [66] and cut 12,000 jobs. Each CEO's decision to protect the highly profitable PC chip business was rational in isolation. [64]

BlackBerry: Co-CEOs dismissed the iPhone as "an entertainment device." An internal 2010 report found buyers increasingly favored touch-only devices — ignored. Consensus-based decision-making among VPs meant "gaining consensus to get something done was next to impossible... It just stalls all innovation." [67] Each quarter, maintaining the enterprise security focus was "not entirely misguided," but collectively, the failure to pivot was fatal.

Google+: Launched June 2011 with forced integration across Gmail, YouTube, and Google Maps. [68] Reality: 90% of user sessions lasted fewer than 5 seconds. [69] Each separation of a feature (Photos, Hangouts) was individually logical ("these are stronger as standalone products") but collectively hollowed out Google+'s value proposition. Shut down April 2019. [70]

Cross-cutting pattern

In none of these cases was there a board meeting where someone said "let's abandon our strategy." Each strategy died through accumulated budget cuts, priority shifts, staff reassignments, and scope narrowing — with leadership maintaining public commitment long after internal actions had effectively killed it.

Sources: TechCrunch (2015); Computerworld; MIT Sloan Management Review ("The Real Lessons from Kodak's Decline"); INSEAD Knowledge ("Who Killed Nokia? Nokia Did"); Slate ("What Happened to Watson Health?"); PCWorld; Failory.

5. The numbers: quantitative evidence on strategy execution and resource allocation

Strategy execution failure rates

- Companies deliver only 63% of the financial performance their strategies promise, [71] with 37% lost to inadequate resourcing (7.5%), poorly communicated strategy (5.2%), unclear action plans (4.5%), blurred accountabilities (4.1%), and other breakdowns. Source: Michael Mankins & Richard Steele, "Turning Great Strategy into Great Performance," HBR, [72] July–August 2005. Research by Marakon Associates. [71] This is the most methodologically robust execution-gap statistic.

- The commonly cited "90% of strategies fail" traces to a 1990s Fortune cover story about prominent CEO failures. The original finding was that 70% of those specific failures were caused by bad execution — a biased sample frequently cited out of context. [73] (Kaplan & Norton, The Balanced Scorecard, 1996; Renaissance Solutions survey, 1996.)

- 61% of executives acknowledge their firms struggle to bridge the gap between strategy formulation and implementation [1] (Economist Intelligence Unit). [74]

- Only 10% of organizations achieve at least two-thirds of their strategic objectives [1] (multiple sources compiled in ClearPoint Strategy).

McKinsey's resource allocation inertia research

This is the most compelling quantitative evidence for the "strategic starvation" mechanism. Stephen Hall, Dan Lovallo, and Reinier Musters analyzed 1,616 US-listed companies over 15 years (1990–2005) using Compustat data: [75][75]

- For one-third of business units, capital received in a given year was almost exactly what was received the year before — mean correlation of 0.99. [76] Across the full economy, the mean correlation was 0.92. [75][75] Budgets barely move regardless of strategy.

- 83% of executives name resource reallocation as the top management lever for spurring growth — yet a third of companies reallocate a mere 1% of capital year-over-year. The average is 8%. [77]

- Companies in the top third of resource reallocators earned 30% higher total shareholder returns annually than those in the bottom third. [76] After 15 years, dynamic reallocators were worth 40% more. [75][75]

- In a 2016 survey of 1,271 executives, only about 30% said their current budgets were similar to their companies' most recent strategic plans. [78][79]

- A 2023 McKinsey survey of 617 executives found only about half say their companies effectively align budgets with corporate strategies. [80] Just 53% say their organizations fully fund the priorities they've identified. [81][80]

Source: Hall, Lovallo & Musters, "How to Put Your Money Where Your Strategy Is," McKinsey Quarterly, March 2012; Atsmon, "How Nimble Resource Allocation Can Double Your Company's Value," McKinsey, August 2016; McKinsey Global Survey on Resource Allocation, October 2023.

The cost of short-termism

The McKinsey Global Institute's Corporate Horizon Index (2017) studied 615 large and mid-cap US companies from 2001–2015. [82] Long-term-oriented companies versus short-term peers showed:

- Revenue grew cumulatively 47% more [82]

- Earnings grew 36% more [83]

- Economic profit grew 81% more [84]

- Market capitalization grew $7 billion more on average [82]

- R&D spending was 50% higher, growing at 8.5% annually vs. 3.7% [82]

- 87% of executives reported pressure to deliver strong short-term results [85]

Strategy attention deficit

- 85% of leadership teams spend less than one hour per month discussing strategy; 50% spend no time at all (Kaplan & Norton / HBR, 2005). [86]

- Only 5% of employees understand their company's strategy [1] (Kaplan & Norton, 1996). [3]

- 60% of organizations don't tie financial budgets to strategic priorities (HBR). [87]

- 45% of ~800 executives reported that strategic planning processes failed to track execution of strategic initiatives [86] (McKinsey, 2006). [86][88]

Innovation allocation gap

Bansi Nagji and Geoff Tuff ("Managing Your Innovation Portfolio," HBR, May 2012) found outperforming firms allocate roughly 70% of innovation resources to core, 20% to adjacent, and 10% to transformational initiatives — but returns follow an inverse ratio: approximately 70% of returns come from transformational innovation, despite receiving only 10% of resources. [89] An Innovation Leader/KPMG survey of 270 Fortune 1000 executives (2018) found companies had shifted to approximately 50-30-20, investing more in adjacent and transformational than the 70-20-10 guideline [90] — though practitioners note teams frequently mislabel incremental work as "adjacent" or "transformational." [91]

6. Mental models and named concepts for the LinkedIn audience

The tyranny of the urgent over the important

Originates from Charles E. Hummel's 1967 booklet Tyranny of the Urgent [92] (over 1 million copies in print). [93] Core insight: "Your greatest danger is letting the urgent things crowd out the important." Connects to Eisenhower's urgent-important distinction, Covey's matrix, and Kotter's true vs. false urgency. [92] PwC's 2026 Global CEO Survey found CEOs spend 47% of their time on issues with a time horizon of less than one year, versus just 16% on issues more than five years out.

The behavioral evidence: Meng Zhu, Yang Yang, and Christopher K. Hsee demonstrated the "mere urgency effect" (Journal of Consumer Research 45(3): 673–690, 2018) — people consistently choose time-sensitive tasks over more important ones even when the time-sensitive tasks offer objectively lower rewards. [92] This violates dominance. [94] The effect is more pronounced among people who perceive themselves as busy. [95]

Hyperbolic discounting applied to organizations

From Richard Herrnstein's matching law (1960s), [96] formalized by David Laibson (1997). Hyperbolic discounting causes valuations to fall very rapidly for near-term delays but slowly for longer delays, creating time inconsistency — plans made for the future get reversed when the future becomes the present. A Stanford King Center working paper found that hyperbolic discounted present value results in "an underinvestment problem for the firm." [97] Applied to organizations: each quarter, the CEO who cuts a training budget to boost short-term profits makes a "rational" decision. But the accumulated effect — higher turnover, reduced innovation capacity — materializes on a timeline that falls outside the discounting window of each individual decision. [98]

The competency trap

Barbara Levitt and James G. March, "Organizational Learning," Annual Review of Sociology 14: 319–340 (1988). [99] A competency trap occurs when favorable performance with an inferior procedure leads an organization to accumulate more experience with it, thus keeping experience with a superior procedure inadequate to make it rewarding to use. [100] The organization gets better at what it already does, which makes current practices look increasingly good relative to untried alternatives — even when those alternatives have higher potential. [101] Related: Dorothy Leonard-Barton's "core rigidities" (1992) — how core capabilities gradually solidify due to path dependence, cognitive lock-in, resource stickiness, and cultural inertia. [102]

Exploration vs. exploitation

James G. March, "Exploration and Exploitation in Organizational Learning," Organization Science 2(1): 71–87 (1991) [103] — one of the most cited papers in organizational theory. March's central argument: "Adaptive processes, by refining exploitation more rapidly than exploration, are likely to become effective in the short run but self-destructive in the long run." [104][105] Exploitation yields returns that are certain, proximate, and measurable. Exploration yields returns that are uncertain, distant, and diffuse. [106].pdf) Organizations naturally drift toward exploitation because its benefits are easier to attribute and defend in any given budget cycle.

The myopia of learning

Daniel Levinthal and James March, "The Myopia of Learning," Strategic Management Journal 14(S2): 95–112 (1993). Organizational learning is subject to three forms of myopia: temporal (sacrificing the long run for the short run), spatial (focusing on what's near over what's far), and failure myopia (learning more from success than failure, leading to overconfidence). These arise from rational responses to complexity — simplification and specialization — but systematically produce short-sighted behavior. [107].%20Strategic%20Management%20Journal%2014%2095-112.pdf)[108]

De-escalation through neglect

While Barry Staw's escalation of commitment (1976) describes doubling down on failing strategies, the inverse is equally damaging and less studied. Organizations can de-escalate strategic commitments not through explicit decisions to withdraw, but through gradual neglect: this quarter's budget is trimmed slightly, a key hire is deferred, a meeting is postponed, a deadline is extended. No single decision looks like withdrawal, but the cumulative effect is that the strategic initiative withers. This connects to the concept of "pluralistic ignorance" — dissenters believe they're alone in their reservations and stay silent. [109]

Structural inertia

Michael T. Hannan and John Freeman, "Structural Inertia and Organizational Change," American Sociological Review 49(2): 149–164 (1984). Organizations achieve reliability and accountability through reproducible structures — but the same capacity creates deep resistance to change. [110] Internal pressures (sunk costs, information filters, political constraints, norms) and external pressures (legal barriers, legitimacy requirements) produce inertia. From population ecology: the same properties that make organizations reliable make them rigid. [111].PDF)

Path dependence

Paul David, "Clio and the Economics of QWERTY," American Economic Review (1985); applied to organizations by Schreyögg & Sydow (2011). Past experiences, routines, and structures constrain future options through self-reinforcing mechanisms: increasing returns to current practices, cognitive lock-in, resource stickiness, and cultural inertia. [112] Each small decision creates a slightly narrower set of future options. [101]

The boiling frog

Popularized in business by Peter Senge in The Fifth Discipline (1990). [113] Despite being scientifically debunked as biology, the metaphor endures: [114] organizations acclimate to gradual changes that eventually prove catastrophic. [115] Their internal sensing mechanisms detect sudden changes but are blind to slow, incremental degradation. [116] Senge used it to describe American automakers ignoring Japanese competition growing from 4% to over 40% market share between the 1960s and 1980s. [113]

7. A unified synthesis for the LinkedIn post

The research converges on a single mechanism operating across cognitive, learning, structural, and strategic levels:

At the cognitive level, the mere urgency effect and present bias cause decision-makers to favor proximate, certain, visible payoffs over distant, uncertain ones — even when the distant payoffs are objectively superior. [117] At the learning level, competency traps, [100] exploitation bias, and the myopia of learning show how organizational learning processes themselves create systematic underinvestment in the future. [108] At the structural level, structural inertia, path dependence, and resource allocation inertia [118] (McKinsey's 0.92 year-over-year budget correlation) [75][75] show how organizational routines resist change through self-reinforcing mechanisms. At the strategic level, Johnson's strategic drift describes the macro-pattern: incremental decisions that appear rational individually accumulate into a widening gap between the organization and its environment. [119]

The critical unifying insight — and the strongest hook for a LinkedIn post — is this: no single decision is irrational. Each individual choice to exploit rather than explore, to address the urgent rather than the important, to invest in known competencies rather than unknown ones, to allocate resources as last year, is defensible in isolation. It is only in aggregate, over time, that these individually rational micro-decisions accumulate into strategic failure. The strategy is never killed. It is hollowed out from within, one reasonable decision at a time.

The most quotable framing comes from Christensen: "Strategy is determined by what comes out of the resource allocation process, not by the intentions and proposals that go into it." [29] And from McKinsey's data: when one-third of companies reallocate just 1% of capital year-over-year, the strategy deck is theater. The real strategy is the budget — and the budget barely moves.

- JBOMS — https://jboms.com/consulting/why-90-of-strategies-fail-real-strategy-execution-failure-examples/

- ResearchGate — https://www.researchgate.net/publication/7715812_Turning_great_strategy_into_great_performance

- Quantive — https://quantive.com/resources/articles/strategy-failure

- Taylor & Francis — https://www.tandfonline.com/doi/full/10.1016/j.polsoc.2010.12.001

- utexas — https://texaspolitics.utexas.edu/archive/html/bur/features/0303_02/muddling.html

- Course Hero — https://www.coursehero.com/lit/The-Science-of-Muddling-Through/plot-summary/

- Studocu — https://www.studocu.com/row/document/sveuciliste-u-zagrebu/e-business/lindblom-c-1959-the-science-of-muddling-through/16528072

- Taylor & Francis — https://www.tandfonline.com/doi/full/10.1016/j.polsoc.2010.12.006

- ERIC — https://eric.ed.gov/?id=EJ223520

- Oxford Academic — https://academic.oup.com/policyandsociety/article/30/1/41/6422278

- Journalism University — https://journalism.university/journalistic-writings/lindbloms-incremental-approach-public-policy/

- Studocu — https://www.studocu.com/in/document/banaras-hindu-university/ba-hons-social-sciences/decision-making-mixed-scanning-theory/26790975

- Wikipedia — https://en.wikipedia.org/wiki/Incrementalism

- ScienceDirect — https://www.sciencedirect.com/science/article/abs/pii/S1449403510000548

- SAGE Publications — https://sk.sagepub.com/ency/edvol/encyclopedia-of-management-theory/chpt/logical-incrementalism

- Oxford Academic — https://academic.oup.com/policyandsociety/article/30/1/29/6422231

- ScienceDirect — https://www.sciencedirect.com/topics/social-sciences/incrementalism

- Mindtools — https://www.mindtools.com/axtnhs8/emergent-strategy/

- SMS +2 — https://sms.onlinelibrary.wiley.com/doi/10.1002/smj.4250090107

- Bartleby — https://www.bartleby.com/essay/Strategic-Drift-P3C9ZXSDJK8Q

- ResearchGate — https://www.researchgate.net/publication/272184191_Strategic_Drift

- Cascade — https://www.cascade.app/blog/strategic-drift

- Empiraa — https://www.empiraa.com/blog/the-four-stages-of-strategic-drift

- Davidpublisher — https://www.davidpublisher.com/Public/uploads/Contribute/5508f990527d3.pdf

- Lucid — https://lucid.co/blog/the-causes-of-strategic-drift-and-how-to-avoid-them

- I-nexus — https://blog.i-nexus.com/what-is-strategic-drift

- Cambridge Core — https://www.cambridge.org/core/books/abs/strategy-and-organization/organizational-culture-and-strategic-change-processes/6A175EBEE082A043F038BCD5469752A4

- LinkedIn — https://www.linkedin.com/pulse/strategic-drift-tanya-sammut-bonnici

- Readingraphics — https://readingraphics.com/book-summary-the-innovators-solution/

- Medium — https://medium.com/keqius-management-notes/the-innovatorss-dilemma-7f36f5e7af94

- Medium — https://medium.com/version-1/the-innovators-dilemma-6de68da8fabc

- Goodreads — https://www.goodreads.com/author/quotes/1792.Clayton_M_Christensen?page=14

- Goodreads — https://www.goodreads.com/work/quotes/138639-the-innovator-s-solution-creating-and-sustaining-successful-growth

- SWE — https://swe.org/magazine/innovators-dilemma/

- Mark Wilson — https://www.markwilson.co.uk/blog/2011/08/the-theory-of-disruptive-innovation-from-the-innovators-dilemma.htm

- Goodreads — https://www.goodreads.com/author/quotes/1792.Clayton_M_Christensen?page=3

- ResearchGate — https://www.researchgate.net/publication/227649297_A_Process_model_of_strategic_business_exit_Implications_for_an_evolutionary_perspective_on_strategy

- SMS — https://sms.onlinelibrary.wiley.com/doi/abs/10.1002/smj.4250171012

- Smoak Signals — https://anthonysmoak.com/2016/03/27/andy-grove-and-intels-move-from-memory-to-microprocessors/

- SAGE Publications — https://journals.sagepub.com/doi/10.2307/3094808

- Oxford University Press — https://global.oup.com/academic/product/from-resource-allocation-to-strategy-9780199277445?lang=3n&cc=jp

- Harvard Business Review — https://hbr.org/1999/07/why-good-companies-go-bad

- Medium — https://medium.com/@bouguerra_70679/product-management-lesson-1-b153ca97aea3

- ResearchGate — https://www.researchgate.net/publication/12761861_Why_Good_Companies_Go_Bad

- London Business School — https://www.london.edu/think/the-essential-don-sull

- Innovationgrowthlab — https://www.innovationgrowthlab.org/about/research-network/people/donald-sull

- Medium — https://medium.com/bc-digest/why-windows-phone-failed-and-how-they-couldve-saved-it-35efc19861ee

- The CDO TIMES — https://cdotimes.com/2025/08/13/case-study-strategic-backstory-nokias-rise-and-fall/

- Medium — https://medium.com/@carsten.krause/microsofts-nokia-acquisition-bold-vision-brutal-outcome-nokia-was-the-mobile-phone-powerhouse-68e038d7e076

- TechSpot — https://www.techspot.com/news/102922-decade-later-how-microsoft-flushed-76-billion-down.html

- Slidebean — https://slidebean.com/story/microsoft-nokia-acquisition

- quartr — https://quartr.com/insights/edge/the-dilemma-that-brought-down-kodak

- Stratrix — https://www.stratrix.com/vault/nokia-smartphone-failure

- Wikipedia — https://en.wikipedia.org/wiki/Microsoft_Mobile

- Henrico Dolfing — https://www.henricodolfing.ch/en/case-study-20-the-4-billion-ai-failure-of-ibm-watson-for-oncology/

- Taylor & Francis — https://www.taylorfrancis.com/books/mono/10.4324/9781003491590/rise-fall-explorys-ibm-watson-health-doug-meil

- Fierce Healthcare — https://www.fiercehealthcare.com/tech/ibm-sells-watson-health-assets-to-investment-firm-francisco-partners

- Slate — https://slate.com/technology/2022/01/ibm-watson-health-failure-artificial-intelligence.html

- Nelson Advisors Blog — https://www.healthcare.digital/single-post/ibm-watson-was-once-heralded-as-the-future-of-healthcare-ai-what-exactly-went-wrong

- Medium — https://medium.com/@averageguymedianow/what-happened-to-ibm-watson-the-rise-fall-and-rebirth-of-ais-most-hyped-technology-28399bb39782

- MM+M — https://www.mmm-online.com/home/channel/features/where-watson-went-wrong/

- AppleInsider — https://appleinsider.com/articles/16/04/30/intel-splits-on-atom-after-the-mobile-relevance-of-x86-whacked-by-apples-ax

- Android Authority — https://www.androidauthority.com/intel-and-the-mobile-market-689064/

- Google Translate — https://translate.google.com/translate?u=https://www.extremetech.com/computing/227816-how-intel-lost-the-mobile-market-part-2-the-rise-and-neglect-of-atom&hl=id&sl=en&tl=id&client=srp

- Network World — https://www.networkworld.com/article/951181/how-intel-knocked-itself-out-of-the-smartphone-chip-market.html

- PCWorld — https://www.pcworld.com/article/414673/intel-is-on-the-verge-of-exiting-the-smartphone-and-tablet-markets-after-cutting-atom-chips.html

- WP Fastest Cache — https://www.wpfastestcache.com/blog/blackberry-the-fall-of-a-tech-giant/

- Wikipedia — https://en.wikipedia.org/wiki/Google+

- Appleton Creative — https://www.appletoncreative.com/why-did-google-plus-shut-down/

- EM360Tech — https://em360tech.com/tech-articles/what-happened-google-why-googles-social-circles-failed

- PubMed +2 — https://pubmed.ncbi.nlm.nih.gov/16028817/

- Harvard Business Review — https://store.hbr.org/product/turning-great-strategy-into-great-performance/R0507E?sku=R0507E-PDF-ENG

- Excitant — https://www.excitant.co.uk/do-9-out-of-10-strategies-fail/

- HBS Online +2 — https://online.hbs.edu/blog/post/why-do-strategic-plans-fail

- mckinsey — https://www.mckinsey.com/capabilities/strategy-and-corporate-finance/our-insights/how-to-put-your-money-where-your-strategy-is

- McKinsey & Company — https://www.mckinsey.com/client_service/corporate_finance/latest_thinking/mckinsey_on_finance/~/media/8D1241628C124B62AC30DAA476B6FF39.ashx

- McKinsey & Company — https://www.mckinsey.com/capabilities/strategy-and-corporate-finance/our-insights/how-nimble-resource-allocation-can-double-your-companys-value

- McKinsey & Company — https://www.mckinsey.com/capabilities/strategy-and-corporate-finance/our-insights/the-finer-points-of-linking-resource-allocation-to-value-creation

- McKinsey & Company — https://www.mckinsey.com/capabilities/strategy-and-corporate-finance/our-insights/keep-calm-and-allocate-capital-six-process-improvements

- McKinsey & Company — https://www.mckinsey.com/capabilities/strategy-and-corporate-finance/our-insights/tying-short-term-decisions-to-long-term-strategy

- McKinsey & Company — https://www.mckinsey.com.br/capabilities/strategy-and-corporate-finance/our-insights/tying-short-term-decisions-to-long-term-strategy

- McKinsey & Company — https://www.mckinsey.com/featured-insights/long-term-capitalism/where-companies-with-a-long-term-view-outperform-their-peers

- McKinsey & Company — https://www.mckinsey.com/mgi/media-center/the-case-against-corporate-short-termism

- Consultancy.uk — https://www.consultancy.uk/news/13089/companies-with-a-longterm-strategy-significantly-outperform-their-rivals

- Milken Institute Review — https://www.milkenreview.org/articles/the-case-against-corporate-short-termism

- Clearpoint Strategy — https://www.clearpointstrategy.com/blog/strategic-planning-statistics

- Funding for Good — https://fundingforgood.org/statistics-about-strategic-planning/

- McKinsey & Company — https://www.mckinsey.com/capabilities/strategy-and-corporate-finance/our-insights/how-to-improve-strategic-planning

- Harvard Business Review — https://hbr.org/2012/05/managing-your-innovation-portfolio

- PR Newswire — https://www.prnewswire.com/news-releases/new-research-shows-need-for-transformational-innovation-and-transformed-business-models-300666328.html

- Umbrex — https://umbrex.com/resources/frameworks/strategy-frameworks/innovation-ambition-matrix/

- 311 Elm Street — http://www.harringtonbrands.com/theblog/2026/3/29/tyranny-of-the-urgent

- Goodreads — https://www.goodreads.com/book/show/20571467-tyranny-of-the-urgent

- Oxford Academic — https://academic.oup.com/jcr/article-abstract/45/3/673/4847790

- Purdue — http://www1.psych.purdue.edu/~gfrancis/Classes/PSY392/ZhuEtAl2018.pdf

- Wikipedia — https://en.wikipedia.org/wiki/Hyperbolic_discounting

- King Center on Global Development — https://kingcenter.stanford.edu/publications/working-paper/firm-investment-decisions-under-hyperbolic-discounting

- Behavioraleconomicsinmarketing — https://behavioraleconomicsinmarketing.com/hyperbolic-discounting-overcoming-short-term-thinking-in-leadership-decisions-transcript/

- Pbworks — https://sjbae.pbworks.com/f/levitt_march_1988.pdf

- Archive — https://ia802305.us.archive.org/23/items/15341_Readings/15341_Readings/Organizational_Learning_and_Change/Levitt_March_Org_Learning_text.pdf

- Stuvia — https://www.stuvia.com/doc/361641/summary-levitt-en-march-1988-organizational-learning

- Journal of Business and Social Sciences — https://iuojs.intimal.edu.my/index.php/intijournal/article/download/718/718

- INFORMS — https://pubsonline.informs.org/doi/10.1287/orsc.2.1.71

- IDEAS/RePEc — https://ideas.repec.org/a/inm/ororsc/v2y1991i1p71-87.html

- ResearchGate — https://www.researchgate.net/publication/235737533_The_Myopia_of_Learning

- Ntnu — http://www.iot.ntnu.no/innovation/norsi-pims-courses/Levinthal/March%20(1991

- Sjsu — http://strategy.sjsu.edu/www.stable/pdf/Levinthal,%20D.%20A.%20and%20J.%20G.%20March%20(1993

- IDEAS/RePEc — https://ideas.repec.org/a/bla/stratm/v14y1993is2p95-112.html

- Aaron Hall — https://aaronhall.com/escalation-of-commitment-the-downfall-of-failing-strategies/

- Semantic Scholar — https://www.semanticscholar.org/paper/Structural-Inertia-and-Organizational-Change-Hannan/ef6388bd6e27ae56054e3a2aa58cda91842ef729

- Ntnu — http://www.iot.ntnu.no/innovation/norsi-pims-courses/harrison/Hannan%20&%20Freeman%20(1984

- Sage Journals — https://journals.sagepub.com/doi/10.1177/0170840610397481

- Stoicacademia — https://stoicacademia.com/2021/10/09/the-business-boiled-frog-phenomenon/

- Sagaleadership — https://www.sagaleadership.com/blog/management-myth-busted-the-boiled-frog

- LinkedIn — https://www.linkedin.com/pulse/5-parable-boiled-frog-its-relevance-organizational-change-dastanboo

- LinkedIn — https://www.linkedin.com/pulse/boiling-frog-syndrome-ayodeji-onabanjo

- Behavioral Economics — https://www.behavioraleconomics.com/resources/mini-encyclopedia-of-be/present-bias/

- McKinsey & Company — https://www.mckinsey.com/capabilities/strategy-and-corporate-finance/our-insights/biases-in-decision-making-a-guide-for-cfos

- PHD Essay +3 — https://phdessay.com/strategic-drift/

Commissioned from our research desk. Subject to final editorial discretion.