The proof is indisputable.

I spent the weekend reading post-mortems on failed mergers. One number keeps sticking with me.

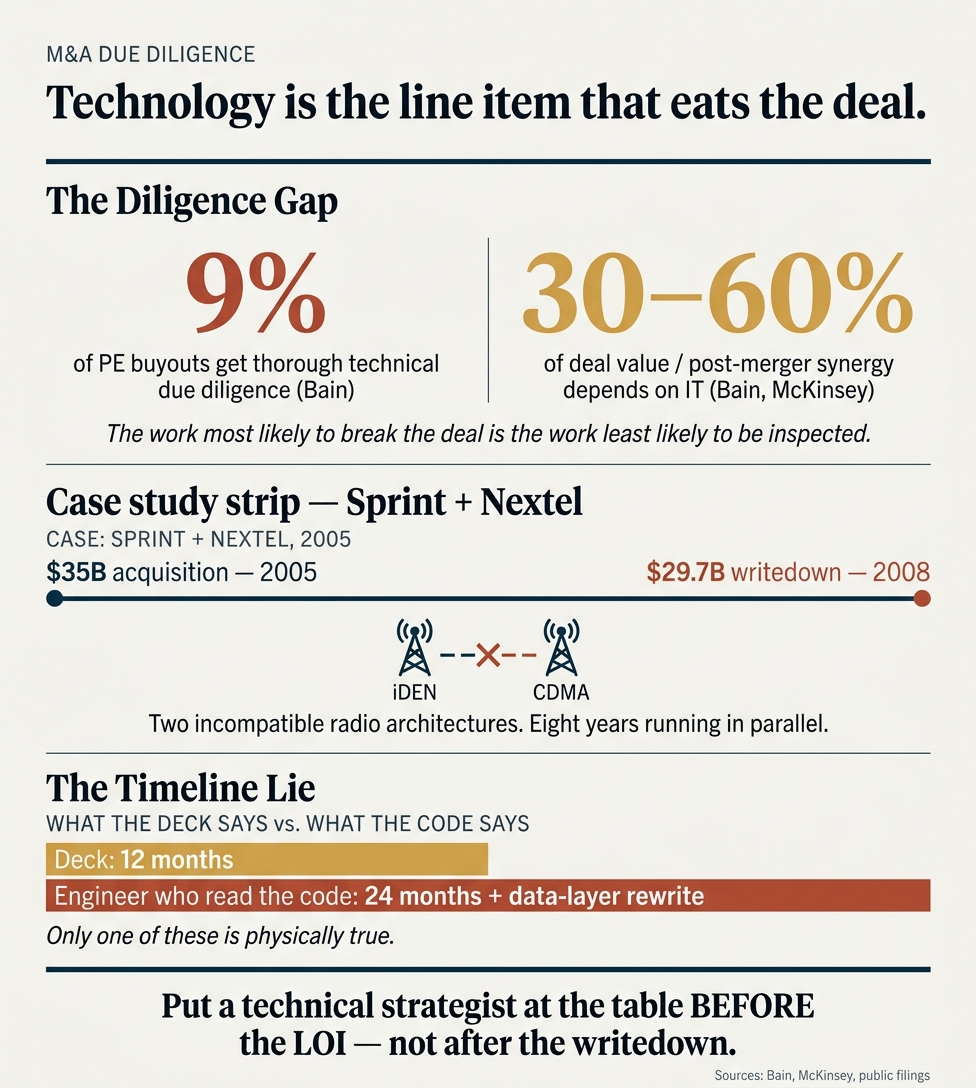

Bain found that thorough technical due diligence happens in about 9% of private equity buyouts. In the same research, they estimated technology drives 30 to 40% of unrealized value in a typical target. McKinsey pegs 50 to 60% of post-merger synergies as IT-dependent.

So the work most likely to make or break the deal is the work least likely to be inspected before signing.

Take Sprint and Nextel. $35 billion deal in 2005, $29.7 billion writedown by 2008. The cause was radio. Nextel ran iDEN, Sprint ran CDMA, two incompatible network architectures that could not be fused without rebuilding one of them from scratch. The financial model assumed subscribers would migrate. The physics said otherwise. Sprint ended up running both networks in parallel for eight years before finally turning iDEN off.

I see the same pattern on smaller deals. A target with a tightly coupled monolith, ten million lines of code, customer logic fused with billing fused with auth. The deck says "integration in 12 months." The engineer who actually reads the code says 24 months with a rewrite of the data layer. Those two numbers are not a negotiation. Only one of them is physically true.

Business due diligence treats technology as a cost line. You find a number, you plug it into the model, you close the deal. Technical due diligence treats it as a structural constraint. Some integrations are possible. Some are possible but expensive. Some are impossible at any price, because the systems were built on assumptions that do not compose.

In healthtech, this gets louder. An acquired EHR with a different FHIR extension set and a different LOINC mapping is a multi-year clinical informatics program where patient safety rides on every edge case. The Oracle-Cerner VA rollout had an "unknown queue" that silently dropped clinical orders. 149 patients were harmed. That is integration debt the diligence process never surfaced.

What I would ask every deal team to change: get your head of engineering, or whoever actually reads the code, into the conversation before the LOI is signed. A two-week pre-LOI technical read is cheap. A ten-billion-dollar goodwill writedown is not.

The question is whether you find out the value of a technical strategist during diligence, or during the writedown.

The silent architecture tax on M&A deal value

Technical strategy is the single most underweighted variable in M&A outcomes. The research below compiles statistics, named studies, documented case studies, and expert commentary to support a LinkedIn post aimed at senior engineering leaders (VPs Eng, CTOs, Directors of Technical Strategy, Principal Engineers), with a healthtech slant. It is organized by the seven research areas requested. Numbers are accompanied by sources, dates, and caveats about quality where warranted.

1. M&A failure rates and the role of technology integration

The "70–90% fail" statistic — origin and nuance

- Harvard Business Review, long-cited: "Study after study puts the failure rate of mergers and acquisitions somewhere between 70% and 90%." [1] The HBR statistic is drawn from decades of academic work, most prominently cited by Roger Martin and Clayton Christensen ("The Big Idea: The New M&A Playbook," HBR, March 2011).

- KPMG's foundational 1999 study ("Unlocking Shareholder Value: The Keys to Success") assessed 700 cross-border deals and found 83% failed to produce any shareholder value, with 53% actively destroying it.

- McKinsey "Perspectives on Merger Integration," 2010: "42% of the time, due diligence conducted before a merger failed to provide an adequate roadmap for capturing synergies." [2] Acquirers see sales decline ~8% in the quarter after announcing a deal. [3]

Tech integration as an attributed failure cause

- Accenture 2002 "Getting IT Right in M&A" (seminal, still widely cited): 70% of executives who performed IT due diligence reported successful integration, vs. 18% of those who did not. [4] 67% said IT was not part of the agenda in early stages — only discussed after public announcement. [4] <50% of acquirers performed detailed IT integration planning. [4] 73% of successful mergers had a full-time IT integration manager, vs. 40% for unsuccessful ones. [4]

- Accenture Strategy 2017 — "Tech-Led Change in M&A" (1,100 C-suite execs, 13 industries, 7 countries): 71% said technology integration determines the success of acquiring progressive targets; Harvard Business Review 84% agreed the CIO should have a seat at the M&A table. [5] Only 7% closed deals with progressive targets in <120 days; 71% took 4–9 months. [5] Accenture claim: a strong IT integration strategy can accelerate synergy capture by up to 25%. [6]

- McKinsey ("Understanding the Strategic Value of IT in M&A"): 50–60% of post-merger synergy initiatives are IT-related; [1] most IT issues are not fully addressed during DD or early PMI. [7] Successful IT integrations yield 10–15% cost savings. [8]

- McKinsey ("The Telltale Signs of Successful Digital Deals"): "Technical due diligence is the single biggest differentiator of deals done well — or poorly."

- Deloitte (widely cited secondary attribution, 2019): >90% of M&A professionals believe IT due diligence is important for deal success. [9]

- Bain & Company 2022 Global Private Equity Report — "Is Your Tech Due Diligence Good Enough?": Technology deals are 31% of all buyouts, but comprehensive tech DD is performed in only ~9% of buyouts generally (closer to 15% for pure-play software). [10] Bain also estimates technology capabilities represent 30–40% of unrealized value in acquisition targets, particularly in traditional industries undergoing digital transformation. [11]

- PwC 2023 M&A Integration Survey: 56% of companies now spend ≥6% of deal value on integration (up from 38% in 2019). [12][13] 21% spend over 10% of deal value on integration (vs. 6% in 2019). [1] 78% of "Most Successful" M&A organizations [13] spent at the ≥6% level [1] vs. 56% of others. [13]

- Industry-reported composite figures (DueDilio citing Deloitte; treat as directional): Technology integration issues account for ~30% of failed mergers; [11] 30–50% of anticipated deal value is lost to slow or ineffective IT integration. [1]

- Windsor Drake, citing industry data: "Only 1 in 4 CEOs report conducting technology due diligence for most of their deals, even though 74% call technology a growth enabler." [14][15]

- Arthur Lawrence, citing a 2,700-respondent IT survey: 65% of respondents reported "buyer's remorse" post-acquisition due to unforeseen cybersecurity issues. [16]

- Bain podcast (Asit Goel, Hank Chen): "It's not sufficient to talk about bits and bytes. It should lead to a conversation about dollars and cents." [17]

- Gartner (Andy Rowsell-Jones): "CIOs face peak integration complexity just when visibility is lowest."

- Baker McKenzie/HBR (Darcy Down, 2024): "The savviest buyers leverage due diligence for integration, because during the diligence phase of the deal, you want to ensure that the synergies sought, and their integration goals, are realistic." [18]

2. Post-merger integration (PMI) timelines and "integration debt"

Typical IT integration timelines

- Full IT integration: 12–18 months minimum for small- and mid-market deals; 2–4 years for R&D-heavy tech companies [1][1] (aggregate of McKinsey/Bain/KPMG PMI benchmarks).

- Accenture: "A full technology integration might take 12–24 months." [15][15] The "golden period" for higher ROI is 1 year; integrations dragging past 2 years show statistically lower ROI. [1]

- Deloitte frames Day 1 as "continuity" only — cybersecurity, cultural, and basic connectivity workstreams [19] — not real IT integration. ERP/CRM consolidation is deferred to later phases.

Overrun rates (how often tech integration blows through plan)

- Gartner: 83% of data migration projects fail or exceed budget/schedule. [20][1]

- Bloor Research: >80% of data migration projects run over time and/or over budget. Cost overruns average 30%. Time overruns average 41%. 64% are delivered late; 37% run over budget.

- PwC-aligned benchmarks: 59% of companies that delayed integration planning experienced cost overruns, vs. 26% of those that didn't. [1]

- KPMG Canada white paper, March 2025 ("Navigating Data Migration in M&A"): Average budget overrun of $0.3 million per data set; [21] >40% of M&A data migration projects face significant challenges; poor data quality can cost businesses up to 35% of operating revenue. [21]

- EY sector benchmarks (2024, % of target revenue spent on integration): Healthcare/Life Sciences 10.1%; Consumer 7.5%; Tech/Media/Telecom 5.6%. [1]

- IT integration cost: ~14% of deal value for deals under $500M; 6–8% for multi-billion-dollar deals [1] (aggregated practitioner benchmark).

"Integration debt" — the emerging construct

- Romulus Strategy (Jason Branin, Dec 2025) — "Integration Debt: The Forgotten Side of M&A": "Like technical debt in software, integration debt is the compound interest of deferred alignment." [22] Three layers:

Systems debt: parallel finance/HR/inventory systems, double data entry, Excel patchwork [22]

Structural debt: unclear decision rights, competing processes, political turf wars [22]

Cultural debt: "us vs. them" resistance, leadership misalignment [22]

- Systems debt: parallel finance/HR/inventory systems, double data entry, Excel patchwork [22]

- Structural debt: unclear decision rights, competing processes, political turf wars [22]

- Cultural debt: "us vs. them" resistance, leadership misalignment [22]

- Example from Romulus: "A manufacturer acquires a logistics firm but leaves separate routing software in place 'temporarily.' Three years later, shipping errors are still being manually reconciled." [22]

- M&A Science podcast (Donara Jaghinyan, 2024): dedicates an episode to "integration debt that piles up when long-tail items don't get done" [23] — "long-tail items get forgotten six months post-close without a formal tracking system." [23]

- Caveat: "integration debt" is not yet formalized in Big 4 playbooks — it's an emerging construct (2024–2025).

Documented failed/abandoned integrations due to architecture mismatches

- TSB / Sabadell (2015–2022) — the single most documented IT migration disaster in banking.

Sabadell acquired TSB in 2015 for £1.7B, [24] with a £450M "dowry" from Lloyds for migration to Sabadell's Proteo4UK core banking platform. Expected savings: £160M/year. [25]

Go-live (April 22, 2018): [26] 1.9M of 5.2M customers locked out; [27] customers saw other customers' accounts; [25] money "disappeared." [28]

Slaughter & May independent review (262 pages): 2,000 defects at go-live; board only told about 800; [29] two data centres were not tested at all. [30]

Total cost impact: ~£200M immediate [29] + £318M migration cost [29] + £176.4M post-migration costs. [25] FCA + PRA fines totaled £48.65M [26][24] (Dec 2022). Former CIO Carlos Abarca personally fined £81,620 [28] (April 2022). CEO Paul Pester resigned. [25][31]

- Sabadell acquired TSB in 2015 for £1.7B, [24] with a £450M "dowry" from Lloyds for migration to Sabadell's Proteo4UK core banking platform. Expected savings: £160M/year. [25]

- Go-live (April 22, 2018): [26] 1.9M of 5.2M customers locked out; [27] customers saw other customers' accounts; [25] money "disappeared." [28]

- Slaughter & May independent review (262 pages): 2,000 defects at go-live; board only told about 800; [29] two data centres were not tested at all. [30]

- Total cost impact: ~£200M immediate [29] + £318M migration cost [29] + £176.4M post-migration costs. [25] FCA + PRA fines totaled £48.65M [26][24] (Dec 2022). Former CIO Carlos Abarca personally fined £81,620 [28] (April 2022). CEO Paul Pester resigned. [25][31]

- Santander / RBS Williams & Glyn (Abandoned 2012): Santander tried to acquire Williams & Glyn branch network; abandoned when complexity of unpicking existing technology became too much [25] (source: Sukand Ramachandran, BCG, via Raconteur).

- Marriott / Starwood (2016, 500M records breached): Marriott chose not to migrate Starwood onto its own reservation system and laid off most of Starwood's IT/security staff. [32] Starwood's legacy system had already been breached in July 2014 (pre-acquisition, undetected for 4+ years, 2 of them post-close). [33] FTC settlement (Oct 2024) + 50-state AG settlement. CSO Online: "Starwood's already-insecure guest reservation system limped on, zombie-like." [34]

- Thrasio (bankruptcy, 2024): acquired 200+ Amazon brands. "Acquired brands faster than it could integrate them… The company was a holding company pretending to be an operating company." [1]

3. Data architecture incompatibility as a deal risk

- KPMG 2025: "A typical M&A deal can involve dozens of data sets; these costs can quickly add up" [21] — $0.3M average overrun per data set + 35% of operating revenue at risk from poor data quality post-close.

- Gartner research note "Mergers and Acquisitions: Integration Without Tears": "Without early and active participation in the strategy phase of a merger and acquisition, technology business unit leaders may get involved too late, putting the company at a competitive disadvantage and deal synergy at risk." [35]

- Gartner (via Gravitas): Poor data quality costs organizations an average of $12.9M annually — a figure that rises significantly in M&A integration contexts. [11]

- Master Data Management: Gartner's MDM Maturity Model highlights that gaps become acute during M&A because "master data touches so many critical business processes." [36] Stibo Systems frames four MDM strategies during M&A — Consolidation, Centralization, Registry, Coexistence — all with different cost profiles.

- Bain 2024 Tech Report: "Failure to integrate the product portfolio was cited as the most common reason why companies were unable to capture revenue synergies." [37] Dealmakers "have massive plugs in the model for these vital longer-term product synergies, with little view into how to actually achieve them." [37]

- Bain on AI-era deals: "The deal multiples are higher, the technology is comparatively unproven, and the value comes from unifying data sets and reinventing offerings." [37]

Data migration as the critical path

- Bloor/TDAN oil & gas case: "Negligence in master data transition" is identified as the primary reason data migration fails during M&A. [38]

- Sprint/Nextel (below) is the canonical example of pure data/architecture incompatibility destroying projected synergies.

- CVS/Aetna: Industry consultant Firoz Vohra: deal success hinges on "speed of integrating vast, disparate pools and streams of consumer, patient and member data." [39] West Monroe's Brad Haller: "Creating this proposed one-stop shop for consumers would cost hundreds of millions and take 18 to 24 months, if not longer." [39]

4. Monoliths and tight coupling as M&A liabilities

Quantified architectural tech debt

- vFunction 2024 survey (>1,000 architecture/dev leaders): U.S. technical debt = $1.52 trillion annually [40] (subset of the $2.41T CISQ poor-software-quality estimate). [41] 51% of organizations allocate >25% of IT budgets to tech debt remediation. Monolithic-architecture companies were 2.1× more likely to experience slow engineering velocity, limited scalability, and poor resiliency than microservices-based peers. [40] (Caveat: vendor-commissioned, but the magnitudes align with independent CISQ.)

Canonical monolith-as-liability case from Bain

- Bain 2022 Global PE Report: Two healthcare-credentialing companies proposed a merger. Company B's customer-facing services "were built on top of an aging, duplicative set of platforms. The overall architecture lacked a single source of truth, and the code was bloated, with tens of thousands of stored procedures and more than 10 million lines of code across seven platforms." [10][10] The finding inverted the deal thesis — Company B's platforms had to be decommissioned, not A's.

- Alvarez & Marsal — "Hidden Threat of Technical Debt in M&A": "Incompatible systems, undocumented code and lack of standardized processes can hinder the seamless integration of the acquired company's technology… risk of hidden costs and extended TSA durations that were not planned for based on diligence findings." [42]

- Allied Venture Partners example: "A fintech startup approaches acquisition… the acquiring company's engineering team identifies a monolithic architecture that would require 18 months of refactoring before integration." [43]

- Martin Fowler (Strangler Fig pattern, 2004): explicitly framed as "a way to manage risk when modernizing or rewriting large, monolithic systems." [44] Now the canonical reference for gradual decomposition used by AWS Prescriptive Guidance, Azure Architecture Center, and M&A integration teams avoiding "big bang" rewrites.

- Sam Newman ("Monolith to Microservices," O'Reilly 2019; QCon London 2020): "The monolith is not the enemy" and "microservices should not be the default choice" [45] — the real goal is independent deployability, the underlying prerequisite for post-merger integration flexibility.

- HealthsystemCIO (2010) on Allscripts/Eclipsys: "When a company like AllScripts buys a suite of products from another firm like Eclipsys, all they can truly integrate are the brochures, PowerPoints, proposals and contracts. The rest is interfaces." [46]

5. Technical due diligence as a discipline

How tech DD is conducted (and where the gap is)

- Bain 2022: "Too many private equity investors still view technology due diligence as a check-the-box exercise." [10] Old model: "bringing a trusted CTO along on a standard diligence assignment to kick the tires in the server room and verify that the ERP and accounting systems weren't a liability." [10] New model: understanding how technology drives performance and risk across the business.

- Crosslake Technologies (tech-DD specialist, 4,000+ prior transactions in its TechIndicators® dataset). [47] Published 8-area checklist: Product strategy & portfolio, Product function & quality, Architecture & code, Processes/practices/tools, People & organization, IT/Operations/DevOps, Product support, Professional services. Sample architecture questions: "Is there anything in the architecture that impedes meeting growth objectives? Are there legacy components requiring replacement? How much will this replacement cost? Are third-party/OSS components problematic legally or technically? Is the code maintainable?" [48]

- Bain's 6-area framework: Product evaluation & roadmap; Technology & architecture; Cybersecurity; Data & analytics; Organization & processes; Technology benchmarking. [10] Bain claims >1,000 tech-DD engagements [49] delivered; acquired Tech Economy (led by Robert Pierce) to scale TDD capability. [50]

- West Monroe "Future of Diligence in PE," 2021 (survey of 100 PE leaders): 68% said they will use more tech-based tools vs. people to conduct diligence. [51] Only ~50% of firms currently transfer diligence findings to operating teams post-close — a major source of value leakage. Works with 40 of top 100 PE firms. [51]

- Automated code-scan vendors (Sema, Vaultinum, RSM): scans for known CVEs, hardcoded credentials, encryption misconfigs, code complexity, architectural anti-patterns, and restrictive OSS license contamination (GPL/AGPL). [52]

Pre-LOI vs post-LOI tech DD

- Traditional: post-LOI DD during ~90-day exclusivity. [53]

- Modern: pre-LOI rapid tech review — "Should we sign the LOI at this valuation?" [54] Crosslake explicitly markets this as a service; [55] Bain reports cases with "two-week exclusivity periods" [56] for TDD.

- McKinsey (Telltale Signs): two cautionary mini-cases — a healthcare-equipment acquirer bought an imaging-tech company whose code was "incompatible with the acquirer's architecture" (avoidable had they tested pre-deal); a communications-hardware maker bought a network-monitoring company whose code was licensed, not owned — the licensor was acquired by a competitor and the code became unavailable. [57]

CTO/CIO role and involvement statistics

- Gartner's 5-criterion decision framework for CIO involvement: (1) IT's role in deal value; (2) integration complexity; (3) availability of IT resources; (4) strategic importance; (5) deal completion likelihood. [58]

- EY 2024 CIO Sentiment Survey: >53% of CIOs say cybersecurity is a top M&A lifecycle challenge. [59][59]

- EY-reported (secondary, DueDilio): 73% of companies that successfully integrate technology in M&A involve their technology integration leadership early in the DD process. [11]

- EY-Parthenon: acquirers can reduce one-time M&A tech integration costs by one-third to one-half in partial integrations using [60] modern tools (including Zero Trust Networks).

- Deloitte 2024 CIO Survey (211 U.S. CIOs): 63% of technology leaders report directly to the CEO [61] (>80% in tech and energy-chemical industries). [62]

- Deloitte 2025 GenAI-in-M&A Survey (1,000 investors): 86% have adopted GenAI in M&A workflows; [63] 35% of GenAI use cases sit in due diligence. [63]

- Crosslake offers interim CIO/CTO/CISO/CPO/Chief Architect placements [64] for PE portfolio companies lacking these leaders for DD and post-close execution.

6. Healthtech-specific integration challenges

Headline healthtech statistics

- KLAS Research Strategic M&A 2019 report (2,176 participants, 67 M&As): 42% of EHR/health-IT vendor M&As result in significant decrease or decrease in customer satisfaction; only 18% see no/minimal change. [65]

- Adler-Milstein & Holmgren (Health Affairs, March 2019) — 4,720 hospitals, 2012–2016 AHA data. [66] Of 88 acquired hospitals, only 35% switched to acquirer's dominant EHR; 44% stayed on a different EHR; [67] 21% already used the dominant vendor. [66] Conclusion: "Claims of EHR system integration as a method to deliver benefits should be taken with healthy skepticism." [66][68]

- Holmgren, Apathy, Kanter (Health Affairs Scholar, Aug 2025): Epic + Oracle Health now cover 71.7% of national inpatient market and 69% of hospital beds [69] — creating "single-point-of-failure" cybersecurity tail risk.

- IBM 2023 Cost of a Data Breach Report: Healthcare breach average >$10M per incident — the highest of any industry (multi-year). [70]

- 84% of hospitals using FHIR APIs continue to struggle with seamless data exchange due to implementation challenges and security vulnerabilities [71] (industry aggregate via ENTER/HIMSS-adjacent sources). Administrative waste despite interoperability standards: $265B–$570B annually. [71]

- EHR purchase/install costs: $15,000–$70,000 per provider [72] (Definitive Healthcare); hospital data-migration costs: "hundreds of millions of dollars and continue with each upgrade." [73]

Regulatory framework

- HIPAA explicitly permits PHI disclosure for M&A due diligence activities (45 CFR), [74] but the Minimum Necessary standard applies, and third-party advisors need BAAs, not just NDAs. [75]

- HIPAA frameworks used in M&A: Affiliated Covered Entity (ACE) — parties become jointly and severally liable for each other's HIPAA violations [76] — or Organized Health Care Arrangement (OHCA), with BAAs as interim solutions.

- Stark Law, Anti-Kickback Statute, state licensing, and reimbursement [77] overlay additional complexity.

Interoperability technical challenges in post-merger healthtech

- Inconsistent LOINC code formats across facility labs (documented "large Midwest health system" delayed integrating lab data into its FHIR-based patient portal). [78]

- Different EHR vendors implement different subsets of FHIR resources with non-standard extensions; [78] legacy HL7 v2 interfaces require heavy remapping.

- Semantic interoperability gaps — "even with the same standards and vocabulary, differences in interpretation arise" [79] (Frontiers in Digital Health, 2024).

- Merging two OMOP Common Data Model instances with different source vocabularies and mappings is a known research-informatics challenge: manual ETL, information loss, constrained datasets.

7. Named case studies with documented technical-integration destruction of value

Ordered by relevance to the LinkedIn audience. All writedown figures and quotes cross-checked against Bloomberg, Reuters, SEC filings, or other primary reporting.

| Deal | Year | Deal value | Writedown/loss | Technical failure mode |

|---|

| Sprint / Nextel | 2005 | $35B | **$29.7B (2008)**goodwill impScribdairment | iDEN vs CDMA — fundamentally incompatible networks; ran two parallel nationwide networks for 8 years until iDEN decommissioned June 2013; lost 4M subscribers in 2008 alone |

| AOL / Time Warner | 2000 | $165B | $99B (2002)— largest ever at the time | Dial-up stack vs broadband/cable infrastructure; no PMI leadership |

| HP / Autonomy | 2011 | $11.1B | $8.8B (2012) | IDOL 7 database not updated in 5 years; CFO Cathie Lesjak admitted she never read the KPMG DD report;~6 hours total conference-call DD for an $11B dealper Lynch's lawyers |

| Teladoc / Livongo | 2020 | $18.5B | $13.4B (2022)goodwill impairment; FY2022 net loss$13.7B | Failed platform integration; exodus of Livongo senior management by Nov 2021;"technical challenges of scaling to different regions"(analyst) |

| Microsoft / Nokia | 2013 | $7.2B | $7.6B (2015)— larger than purchase price | Windows Phone ecosystem failure; 7,800 layoffs |

| Microsoft / aQuantive | 2007 | $6.3B | $6.2B (2012)— caused MSFT's first quarterly loss as a public company | Display-advertising tech sidelined by Bing/search pivot; aQuantive talent drain |

| eBay / Skype | 2005 | $2.6B | $1.4B writedown; sold at ~$2.75B enterprise value | P2P VoIP architecture not integrable with e-commerce; core IP (Joltid) still owned by founders |

| Google / Motorola | 2012 | $12.5B | Sold to Lenovo for**$2.9B in 2014**(~19 months later) | HW/SW culture clash; Google optimized for Android-partner neutrality |

| Yahoo / Tumblr | 2013 | $1.1B | $712M cumulative writedowns (2015–16); sold to Automattic for ~$3M in 2019 | Rolled-back sales integration; ad-monetization blocked by adult content |

| Daimler / Chrysler | 1998 | ~$36B | Chrysler sold to Cerberus 2007 (effectively $7.4B) | Engineering/product systems never consolidated despite SAP/CATIA commonality |

| Cerner / Siemens Health Services | 2014 | $1.3B | 87% of Soarian customers leaving within 2 years (KLAS) | Soarian*"orphaned"*— Cerner explicitly did not acquire it for the platform IP; dual-EMR support burden |

| Oracle / Cerner | 2022 | $28.3B | VA rollout paused April 2023; Oracle cut**~10,000 Cerner roles** | *"Unknown queue"*at Mann-Grandstaff VA routed 11,000+ clinical orders without alerts;≥149 patients harmedper VA IG; live at only6 of 171+ VA medical centersby late 2025;78% of Oracle-Cerner VA userssaid system did not enable high-quality care (KLAS —lowest rating for any EHR surveyed) |

| UnitedHealth / Change Healthcare | 2022 | $13B | $3.09B (2024) cyber loss;190M individualsaffected | Ransomware entered via a Change server without two-factor authentication~18 months post-close; $22M ransom paid; Sen. Ron Wyden:"This hack could have been stopped with cybersecurity 101." |

| Broadcom / VMware | 2023 | $61B | $200B+ in claimed customer churn/lawsuits (AT&T, UnitedHealthcare sued) | Forced subscription bundling;500–600% price increasesat some customers;32% of customers considering leaving(CloudBolt/Wakefield survey) |

| Allscripts / Eclipsys | 2010 | $1.3B | ~$9.75M class action settlement (2015) | Overstated ability to integrate Microsoft .NET/SQL Server with Eclipsys stack; Allscripts exited acute-care market 2022 |

| Quaker / Snapple | 1994 | $1.7B | $1.4B charge (1997) | Not tech — but canonical distribution-integration failure; 300+ independent distributors revolted |

Noteworthy healthtech integration cost overruns not tied to a specific deal failure

- Partners HealthCare (Mass General Brigham) Epic rollout: Budget $600M → $1.2B (doubled) — largest single investment in Partners history. 600 employees/consultants hired; 2,300 extra people for go-lives. Brigham's first budget shortfall in 15+ years: $53M, directly attributed to EHR implementation. Q2 2016 operating loss $33M vs prior-year gain of $30M. MGH CIO Keith Jennings: "A project like this, this is not an IT implementation, this is a business transformation for your clinical systems, your clinical user." Brigham COO Ron Walls: "We would have liked it to be easier for our clinicians to do what they're trying to do… Instead, at the beginning especially, it slowed things down."

- Advocate Aurora / Atrium (2022): Advocate ran Cerner + Allscripts + eClinicalWorks; Aurora ran Epic. Advocate announced switch to Epic to align — project expected to take ~3 years. CIO Bobbie Byrne, MD: "This transition will allow for better interoperability throughout our entire geographic region."

- CVS / Aetna: Industry consultant Adam Fein: "How will the now highly-indebted CVS Health find genuine synergy from its sprawling operations and disparate corporate cultures?" By late 2024, CVS was publicly weighing a breakup — evidence that vertical tech/data integration had not delivered expected synergies.

- Centene / Magellan (2022): Centene divested Magellan Specialty Health to Evolent (~$660M) within ~1 year of closing the $2.2B deal — partial reversal suggests integration failed to deliver thesis value.

Counter-examples (integrations that worked)

- IBM / Red Hat (2019, $34B): Red Hat revenue roughly doubled to ~$6.5B/year by 2024–2025; OpenShift ARR $1.7–1.8B, growing 20%+; software now ~45% of IBM revenue (vs high-20s% in 2018). Key choice: preserved Red Hat independence and culture; no goodwill writedown.

- Oracle / Sun Microsystems (2010, $7.4B): No large goodwill writedown. Oracle President Mark Hurd (Jan 2013): cumulative cash flow "has far exceeded the purchase price."

Conclusion — the synthesis for the post

Three facts, taken together, summarize the argument:

- Tech DD is dramatically undersupplied. Comprehensive tech DD happens in only ~9% of buyouts (Bain 2022), yet 50–60% of post-merger synergies are IT-dependent (McKinsey) and technology drives 30–40% of unrealized value (Bain) in the typical target.

- When architecture is incompatible, the deal thesis inverts. Sprint/Nextel (iDEN vs CDMA → $29.7B writedown), TSB/Sabadell (core banking migration → £48.65M in fines + executive fines + CEO resignation), eBay/Skype (P2P not integrable → sold at a loss), and Bain's healthcare-credentialing case (10M lines of code, 7 platforms → acquirer's roadmap had to be scrapped) all tell the same story.

- In healthtech, architecture risk is existential, not just financial. Oracle/Cerner's VA rollout harmed ≥149 patients via an "unknown queue" in clinical order routing; UnitedHealth/Change Healthcare's post-close security integration gap (no MFA on a core server) created the largest US healthcare data breach ever at 190M individuals and $3.09B in 2024 losses. The Mass General Brigham Epic consolidation doubled from $600M to $1.2B. Only 35% of acquired hospitals successfully switched to the acquirer's dominant EHR (Health Affairs, 2019) — meaning the promised clinical-data unification usually never arrives.

The through-line for a senior engineering audience: business DD treats technology as a cost line item; technical DD treats it as a structural constraint that can make the deal thesis physically impossible to execute. As McKinsey puts it: "Technical due diligence is the single biggest differentiator of deals done well — or poorly." And as Gartner's Andy Rowsell-Jones observes: "CIOs face peak integration complexity just when visibility is lowest." The strategic implication — that CTOs and VPs of Engineering belong in the pre-LOI conversation, not the post-close cleanup — is supported by 24 years of data running from Accenture's 2002 IT-in-M&A study to Deloitte's 2025 GenAI-in-M&A survey.

- pmistack +2 — https://pmistack.com/blog/post-merger-integration-statistics

- McKinsey & Company — https://www.mckinsey.com/~/media/McKinsey/Business%20Functions/Organization/Our%20Insights/Merger%20Manager%20Compendium/A%20McKinsey%20perspective%20on%20creating%20transformation%20value%20and%20mergers.pdf

- IMAA +2 — https://imaa-institute.org/publications/perspectives-on-merger-integration/

- Accenture — https://newsroom.accenture.com/subjects/technology/getting-information-technology-right-is-key-to-ma-successes-according-to-accenture-study.htm

- Harvard Business Review — https://hbr.org/sponsored/2018/05/how-technology-is-changing-ma-in-the-u-s

- Flevy — https://flevy.com/topic/manda/case-telecom-firm-merger-acquisition-strategy-digital-services

- mckinsey — https://www.mckinsey.com/~/media/McKinsey/Business%20Functions/Strategy%20and%20Corporate%20Finance/Our%20Insights/Understanding%20the%20strategic%20value%20of%20IT%20in%20M%20and%2038A/Understanding%20the%20strategic%20value%20of%20IT%20in%20M%20and%2038A.pdf

- McKinsey & Company — https://www.mckinsey.com/capabilities/strategy-and-corporate-finance/our-insights/understanding-the-strategic-value-of-it-in-m-and-38a

- Gravitas — https://www.gravitasconsulting.com/insight/it-m-a-navigating-the-complexities-of-technology-integration

- bain — https://www.bain.com/insights/tech-due-diligence-global-private-equity-report-2022/

- DueDilio — https://www.duedilio.com/technology-due-diligence-in-mergers-and-acquisitions/

- PwC — https://www.pwc.com/us/en/services/consulting/deals/library/successful-mergers-and-acquisitions-organizations.html

- PwC — https://www.pwc.com/us/en/services/consulting/deals/library/ma-integration-survey.html

- Windsor Drake — https://windsordrake.com/technology-due-diligence-in-mergers-and-acquisitions/

- Accenture — https://www.accenture.com/us-en/insights/strategy/mapping-dna-mergers-acquisitions-value

- Arthur Lawrence — https://www.arthurlawrence.net/blog/technology-due-diligence-in-mergers-and-acquisitions/

- Bain & Company — https://www.bain.com/insights/tech-due-diligence-from-bits-and-bytes-to-dollars-and-cents-podcast/

- Baker McKenzie — https://www.bakermckenzie.com/en/newsroom/2024/04/hbr-speaks-to-darcy-down

- Deloitte — https://www2.deloitte.com/us/en/services/mergers-and-acquisitions.html

- Integrate.io — https://www.integrate.io/blog/what-is-data-migration/

- KPMG — https://assets.kpmg.com/content/dam/kpmg/ca/pdf/2025/03/ca-white-paper-on-data-migration-en.pdf

- Substack — https://romulusstrategy.substack.com/p/integration-debt-the-forgotten-side

- Mascience — https://www.mascience.com/podcast/how-integration-debt-cultural-friction-and-communication-failures-kill-m-a-deals

- rte — https://www.rte.ie/news/business/2022/1220/1342872-tsb-fined-by-uk-regulators

- raconteur — https://www.raconteur.net/finance/mergers-acquisitions/failed-mergers-acquisitions/

- Computer Weekly — https://www.computerweekly.com/news/252528519/TSB-hit-with-huge-fine-after-IT-migration-disaster

- Ekco — https://www.ek.co/publications/tsb-migration-disaster/

- Computer Weekly — https://www.computerweekly.com/news/366609580/TSB-systems-could-be-on-the-move-again-as-BBVA-eyes-its-parent

- The Register — https://www.theregister.com/2022/12/20/tsb_fine/

- Tech Monitor — https://www.techmonitor.ai/policy/privacy-and-data-protection/tsb-it-crash-migration-bank-fca

- computerweekly — https://computerweekly.com/news/252528519/TSB-hit-with-huge-fine-after-IT-migration-disaster

- BreachSense — https://www.breachsense.com/blog/marriott-data-breach-case-study/

- Huntress — https://www.huntress.com/threat-library/data-breach/marriott-data-breach

- Hotel Tech Report — https://hoteltechreport.com/news/marriott-data-breach

- Prometheus Group — https://www.prometheusgroup.com/learning-center/merger-and-acquisitions-best-practices-for-master-data

- Gartner — https://www.gartner.com/en/data-analytics/topics/master-data-management

- Bain & Company — https://www.bain.com/insights/technology-m-and-a-report-2024/

- Tdan — https://tdan.com/a-case-study-on-data-migration-strategy-and-template-design-for-mergers-and-acquisitions-in-the-oil-and-gas-sector/14999

- Healthdatamanagement — https://www.healthdatamanagement.com/articles/cvs-aetna-combination-to-face-vast-data-integration-challenges

- itprotoday — https://itprotoday.com/it-operations-and-management/how-technical-debt-can-impact-innovation-and-how-fix-it

- Garnetgrid — https://garnetgrid.com/insights/real-cost-of-technical-debt

- Alvarez & Marsal — https://www.alvarezandmarsal.com/insights/hidden-threat-technical-debt-ma-best-practices-ensure-successful-deal

- Allied — https://www.allied.vc/guides/how-tech-debt-impacts-startup-valuations

- AWS — https://docs.aws.amazon.com/prescriptive-guidance/latest/modernization-aspnet-web-services/fig-pattern.html

- InfoQ — https://www.infoq.com/news/2020/05/monolith-decomposition-newman/

- Healthsystemcio — https://healthsystemcio.com/2010/06/16/can-allscripts-eclipsys-integrate/

- LinkedIn — https://www.linkedin.com/company/crosslake-technologies

- crosslaketech — https://crosslaketech.com/technical-due-diligence-checklist-why-acquiring-firms-need-it/

- Bain & Company — https://www.bain.com/industry-expertise/private-equity/tech-due-diligence/

- Theconsultingreport — https://www.theconsultingreport.com/bain-company-boosts-due-diligence-efficiency-with-tech-economy-acquisition/

- @westmonroe — https://www.westmonroe.com/press-releases/private-equity-firms-change-due-diligence-process-data-value-creation

- Vaultinum — https://vaultinum.com/tech-due-diligence

- LinkedIn — https://www.linkedin.com/pulse/kicking-tires-why-pre-loi-due-diligence-so-important-brad-bonde-cpa

- LBMC — https://www.lbmc.com/blog/pre-loi-due-diligence/

- Crosslake — https://crosslaketech.com/tech-due-diligence/

- Bain & Company — https://www.bain.com/client-results/rapid-tech-due-diligence-helped-a-pe-firm-invest-with-confidence/

- McKinsey & Company — https://www.mckinsey.com/capabilities/mckinsey-digital/our-insights/the-telltale-signs-of-successful-digital-deals

- SDxCentral — https://www.sdxcentral.com/analysis/tips-for-cios-on-where-and-when-to-engage-in-ma-deals/

- EY — https://www.ey.com/en_us/insights/strategy/how-cios-can-supercharge-an-m-and-a-technology-integration

- EY — https://www.ey.com/en_us/insights/strategy-transactions/how-rapid-m-a-it-integration-can-create-deal-value

- Deloitte — https://www2.deloitte.com/us/en/pages/about-deloitte/articles/press-releases/cio-perspectives-new-deloitte-survey-unveils-technology-leaders-current-priorities-performance-and-competencies.html

- PR Newswire — https://www.prnewswire.com/news-releases/cio-perspectives-new-deloitte-survey-unveils-technology-leaders-current-priorities-performance-and-competencies-302162591.html

- Peprofessional — https://peprofessional.com/2025/10/deloitte-pe-loves-ai/

- Crosslake — https://crosslaketech.com/

- Becker's Hospital Review — https://www.beckershospitalreview.com/ehrs/klas-customer-satisfaction-drops-42-after-ehr-vendor-merger-acquisition.html

- Healthcare Innovation — https://www.hcinnovationgroup.com/clinical-it/electronic-health-record-electronic-medical-record-ehr-emr/news/21071375/is-the-link-between-hospital-mergers-and-ehr-consolidation-overstated

- Healthcare IT News — https://www.healthcareitnews.com/news/mergers-and-acquisitions-not-leading-promised-ehr-integration

- Health Affairs — https://www.healthaffairs.org/do/10.1377/hblog20190304.998205/full/

- Oxford Academic — https://academic.oup.com/healthaffairsscholar/article/3/8/qxaf164/8236684

- OSP — https://www.osplabs.com/insights/ehr-consolidation-strategies-in-healthcare-merger-and-acquisitions/

- ENTER — https://www.enter.health/post/hl7-fhir-healthcare-data-interoperability-future

- Definitive Healthcare — https://www.definitivehc.com/blog/EHR-integration-success-post-merger-acquisition

- Definitive Healthcare — https://www.definitivehc.com/blog/healthcare-mergers-acquisitions-ehr-interoperability

- Bowditch & Dewey — https://www.bowditch.com/2023/08/30/corporate-insights-disclosing-phi-upon-the-sale-of-a-medical-practice/

- ByrdAdatto — https://byrdadatto.com/banter/protecting-patient-information-during-health-care-m-and-a/

- Jackscamp — https://www.jackscamp.com/common-hipaa-pitfalls-in-health-care-mergers-and-acquisitions-and-how-to-identify-them/

- Di Pietro Partners — https://ddpalaw.com/healthcare-law/healthcare-m-a-due-diligence/

- Microtek Learning — https://www.microteklearning.com/blog/hl7-fhir-challenges-and-solutions-for-hospitals/

- Frontiers — https://www.frontiersin.org/journals/digital-health/articles/10.3389/fdgth.2024.1480600/full

Commissioned from our research desk. Subject to final editorial discretion.

The underappreciated role of technical strategy in M&A due diligence, specifically how acquiring a company with an incompatible data architecture or deeply coupled monolith can silently destroy the projected value of a deal. Walk through how integration timelines are routinely underestimated because business due diligence treats technology as a line-item cost rather than a structural constraint. Look into studies on M&A failure rates attributed to technology integration challenges and post-merger integration timelines. The takeaway is that a Director of Technical Strategy should have a seat at the table before the LOI is signed, not after the deal closes.