Why structural protection beats strategic clarity

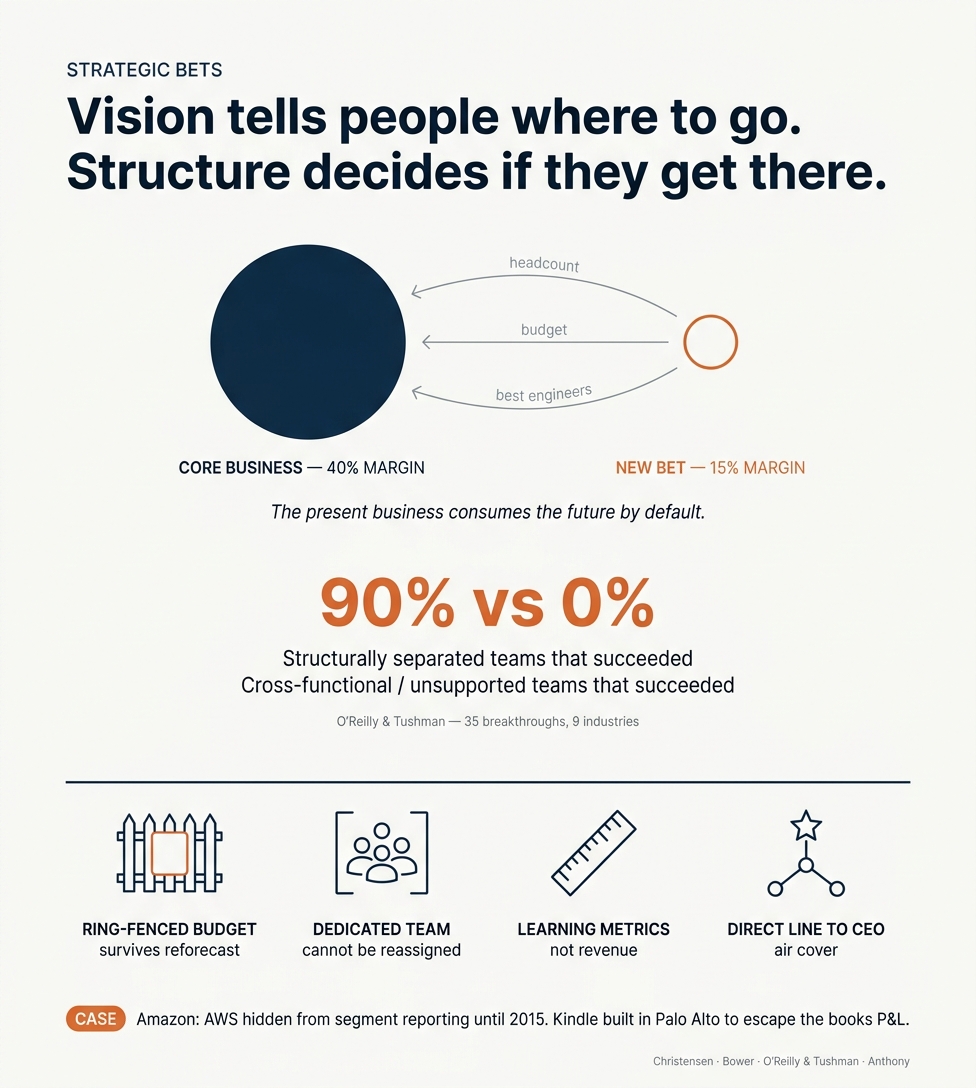

Bottom line: The empirical evidence is overwhelming that strategic clarity alone cannot defend a strategic bet against a profitable core. Across 60 years of management research — Bower/Christensen, O'Reilly/Tushman, Govindarajan/Trimble, Anthony/Innosight, Moore, Blank — the convergent finding is that the new bet survives if and only if it has separate teams, separate budgets, separate metrics, separate governance, and direct CEO-level air cover. The core's resource-allocation process, staffed by rational managers responding to rational incentives, will systematically starve any unprotected disruptive bet. The most quantified data point: in a study of 35 attempts at breakthrough innovation across 9 industries, >90% succeeded under structurally ambidextrous designs; 0% succeeded under cross-functional or unsupported teams (O'Reilly & Tushman, HBR April 2004). This is research material — not a finished post. [1].pdf)

1. The structural asymmetry: why "good strategy" loses to the core

The foundational insight is Joseph Bower's Resource Allocation Process (RAP) theory (1970 HBS book), extended by Christensen (Bower & Christensen, "Disruptive Technologies: Catching the Wave," HBR Jan-Feb 1995; Christensen & Bower, Strategic Management Journal 1996). A company's actual strategy is not what the deck says — it is the sum of thousands of small, decentralized resource decisions made daily by middle managers, sales reps, engineers, and finance staff. Each decision is rational on its own terms. Aggregated, they always favor the existing high-margin business. [2]

Christensen's central claim (from The Innovator's Dilemma, 1997): "Good management itself was the root cause [of failure]. Managers played the game the way it was supposed to be played. The very decision-making and resource-allocation processes that are key to the success of established companies are the very processes that reject disruptive technologies." He concludes: "Companies in fact are specifically organized to under-invest in disruptive innovations." [3][4]

The mechanism is not stupidity or politics — it is rational margin math. If the core earns 40% gross margin, every project must clear that bar to survive the prioritization process. A nascent bet with 15% margins on a small market gets correctly declined at every level. Salespeople on commission rationally call the $5M-deal core customer before the $50K-deal pilot. Best engineers go to largest accounts. Strategy decks demand TAM; disruptive markets don't have measurable TAMs and lose every comparison. [5][6]

Christensen's RPV framework (Innovator's Dilemma Ch. 8; Innovator's Solution Ch. 7) crystallizes why this is structural, not motivational: Resources are flexible (you can hire, fire, reallocate). Processes are inflexible by design — "their very raison d'être is to cause the same thing to be done consistently." Values — the standards by which employees prioritize, including margin thresholds and minimum market size — are the killer. "An organization cannot have multiple sets of values." A 40%-margin organization literally cannot prioritize 15%-margin opportunities. [7][8]

This explains Christensen's blunt prescription (Bower & Christensen, HBR 1995): "The only way to do that is to create organizations that are completely independent of the mainstream business." And from Innovator's Dilemma Ch. 8: "In our studies of this challenge, we have never seen a company succeed in addressing a change that disrupts its mainstream values absent the personal, attentive oversight of the CEO." [9][7]

The deliberate-vs-emergent distinction (Mintzberg & Waters 1985, adapted by Christensen) reinforces this: in disruptive contexts, "plans must serve a very different purpose: they must be plans for learning rather than plans for implementation." A strategy review process built for deliberate execution will reject any project that cannot pre-quantify market size — which is every real disruption. [10]

2. The empirical evidence base: Christensen's cases and their critics

Christensen's foundational evidence base is the disk drive industry (his Harvard PhD). The pattern repeats across architecture transitions: 14-inch → 8-inch (mid-1970s), 8-inch → 5.25-inch (1980), 5.25-inch → 3.5-inch (1984-87). The canonical RAP story: Seagate's engineers built 3.5-inch prototypes in 1985 — two years before Conner Peripherals shipped — but Seagate's marketing organization killed the program after existing IBM/desktop OEM customers showed lukewarm interest. Conner shipped in 1987 with $113M first-year revenue, nearly all from a $30M Compaq investment. [11]

In steel, mini-mills (Nucor, Chaparral) started in rebar (~7% margin) in the mid-1960s. Integrated mills (US Steel, Bethlehem) happily ceded rebar as low-margin, then ceded bar/rod, then structural beams, then sheet steel (Nucor's 1989 Crawfordsville thin-slab plant). At each step, every integrated CFO's spreadsheet correctly showed it was more profitable to retreat upmarket. By 2017, only ~9 integrated mills remained in the US. "No integrated steel company was able to successfully deploy mini-mill technology inside their business model — even with a 20% cost advantage." [12]

The theory has legitimate critiques worth flagging. Jill Lepore's "The Disruption Machine" (New Yorker, June 23, 2014) noted Seagate's sales doubled from 1989 to 1990 to $2.4B — "more than all of its U.S. competitors combined" — so it wasn't actually disrupted. Andrew King & Baljir Baatartogtokh (MIT Sloan Management Review, Fall 2015) tested 77 Christensen cases against four theory elements with 79 industry experts; only 7 cases (9%) fully fit. Their conclusion: "Many of the theory's exemplary cases did not fit its conditions and predictions well." Christensen himself walked back over-applications (the iPhone, Uber) in his December 2015 HBR rejoinder. The takeaway: disruption is one of several incumbent-failure mechanisms, but the resource-allocation insight underlying it is robust independent of whether any specific case is "true disruption." [13]

3. The quantified evidence on structural separation

The strongest empirical work is O'Reilly & Tushman, "The Ambidextrous Organization," HBR April 2004. They studied 35 attempts at breakthrough innovation across 9 industries, classified by four organizational designs. The result, in their own words: "More than 90% of those using the ambidextrous structure succeeded in their attempts, while none of the cross-functional or unsupported teams, and only 25% of those using functional designs, reached their goals." Additionally: "In almost every instance in which an ambidextrous structure was used, the competitive performance of the existing product either increased or held steady." [1].pdf)[14]

Their definition is important: "separate their new, exploratory units from their traditional, exploitative ones, allowing them to have different processes, structures, and cultures; at the same time, they maintain tight links across units at the senior executive level." Separation at the operating level + integration at the top. Not a skunkworks tossed over the fence. [15]

The empirical pattern is reinforced by Innosight's S&P 500 longevity research. Average tenure: 33 years in 1964 → 24 years in 2016 → forecast 12 years by 2027 (Anthony, Viguerie et al., "2018 Corporate Longevity Forecast"). At current churn, roughly half the S&P 500 will be replaced over the next decade. Bain (Zook & Allen, The Founder's Mentality, 2016): only 1 in 9 companies achieves a decade or more of sustained profitable growth. [16]

Caveat on widely-cited stats: "70% of digital transformations fail" (McKinsey) traces back to John Kotter's 1995 HBR change-management work and has been recycled for decades without a single replicable study. "96% of innovation fails" (Doblin/Larry Keeley) lacks a transparent dataset. The defensible quantitative anchors are the O'Reilly/Tushman 35-case study and the Innosight longevity series. CB Insights found 60% of corporate accelerators founded in 2016 had shut down within 24 months — the cleanest analogue to the "18-month reabsorption" intuition the user asked about (a discrete academic literature on innovation reabsorption timing does not appear to exist). [17]

4. Convergent frameworks, identical prescription

Every major framework in the field arrives at the same structural recommendation with different vocabulary:

| Framework (year) | Core | New bet | Linking mechanism |

|---|

| Bower/Christensen (1995-2003) | Mainstream organization | Autonomous independent organization | CEO personal oversight |

| McKinsey 3 Horizons / Baghai-Coley-White (1999) | Horizon 1 | Horizon 3 | Senior leader time + protected resources |

| O'Reilly & Tushman (2004) | Exploitative unit | Exploratory unit | Senior executive team integration |

| Govindarajan & Trimble (2010) | Performance Engine | Dedicated Team | Shared Staff partnership |

| Geoffrey Moore (2015) | Performance Zone | Incubation / Transformation Zone | CEO sponsorship for Transformation |

| Anthony/Gilbert/Johnson (2017) | Transformation A | Transformation B | Capabilities Link / Exchange Teams |

| Steve Blank (2019) | Execution pipeline | Innovation Pipeline | Innovation Doctrine + parallel budget |

Scott Anthony's mantra: "A does A, B does B." Govindarajan: "Innovation is 1% inspiration and 99% perspiration" — execution requires dedicated structure, not enthusiasm. Vijay Govindarajan & Chris Trimble add a vital nuance in The Other Side of Innovation (2010): the Dedicated Team must treat the Performance Engine as a strategic partner, not a competitor — "a positive, persuasive, and collaborative approach to every interaction is necessary." Otherwise the new bet wins the org-chart battle and loses the access-to-capability war. [18]

Geoffrey Moore's Zone to Win (2015, foreword by Marc Benioff) supplies the operating discipline: the Transformation Zone "is piloted directly by the CEO, and it sits at the top of every Exec agenda. This is necessary to overcome that tendency for the Performance Zone to (quite rightly) crush new things." The Incubation Zone "operates independently of the annual financial planning process, offering a safeguarded space… free from the typical constraints associated with standard budgeting." Moore is explicit: "you cannot have two number-one priorities." [19]

Steve Blank's diagnosis of why most attempts fail anyway: "Why Companies Do 'Innovation Theater' Instead of Actual Innovation" (HBR, Oct 2019). His three theater modes: organizational theater (reorgs), innovation theater (hackathons, design thinking workshops, demo days), process theater (reforming procurement/HR without strategy). His one-line indictment: "Execution pays your salary while innovation pays your pension." And: when innovation programs are real, "trying to integrate new, unbudgeted, and unscheduled innovation projects into an engineering organization that has line item budgets for people and resources results in chaos and frustration." His critique of McKinsey's Three Horizons (HBR Feb 2019): the time axis is obsolete; H3 disruption can ship as fast as H1, so structural separation matters even more, not less. [20]

The IBM EBO program is the most rigorously documented success — and a direct template. Under Lou Gerstner / Sam Palmisano with Bruce Harreld (SVP Strategy) running it from 2002: separate reporting line to corporate (not LOB), ring-fenced funding, milestone-based metrics, monthly CEO-level reviews of all seven EBOs, and explicit graduation criteria (leadership team in place, articulated profit path, early market success, proven customer value proposition). 25 EBOs launched 2000–2005 with three failures; the program produced >$15B in incremental revenue (O'Reilly, Tushman & Harreld, California Management Review, 2009). Cisco attempted the same model and failed. [21]

5. Amazon as the working model

Amazon is the most-cited and best-documented case of operationalized structural protection. The mechanisms (from Bryar & Carr, Working Backwards, 2021; Stone, The Everything Store, 2013, Amazon Unbound, 2021; shareholder letters at aboutamazon.com):

AWS origin and protection. Andy Jassy authored the AWS vision document in September 2003 (reportedly 30 drafts); S-Team approved it with ring-fenced funding for ~57 hires. Chris Pinkham and Chris Brown were relocated to Cape Town, South Africa to build EC2 in physical isolation; "EC2 was born in isolation with Pinkham talking to his colleagues in Seattle only sporadically, at least for the first year" (Stone). S3 launched March 14, 2006; EC2 launched August 25, 2006. AWS revenue was deliberately not broken out as a separate segment until Q1 2015 — protecting it from quarterly-earnings scrutiny during the formative money-losing years. First standalone year (2015): $7.88B, +70% YoY. 2024: $107.6B revenue, ~$39.8B operating income (~37% margin), >60% of Amazon's total operating income on ~17% of revenue. Roughly 20x in nine years. [22]

The "single-threaded leader" (STL) concept. Bryar & Carr: "the biggest predictor of a team's success was not whether it was small but whether it had a leader with the appropriate skills, authority, and experience to staff and manage a team whose sole focus was to get the job done… single-threaded leaders and separable, single-threaded teams were born." Jeff Wilke: "Separable means almost as separable organizationally as APIs are for software. Single-threaded means they won't work on anything else." Dave Limp (SVP Devices): "The best way to fail at inventing something is by making it somebody's part-time job." [23]

Kindle. Bezos pulled Steve Kessel — then running the profitable physical books business — entirely off that P&L to lead the new digital one. Bezos to Kessel (Stone, 2013): "Your job is to kill your own business. I want you to proceed as if your goal is to put everyone selling physical books out of a job." Reasoning per Stone: "if the Head of Media was also responsible for the digital media business, the latter would never be a priority due to the lower revenue contribution… the whole initiative would be doomed to fail." Lab126 established 2004 in Palo Alto — geographically separate from Seattle retail. Kindle launched November 2007. [24]

Fire Phone failure (2014). Launched June 18, 2014. Amazon recorded a $170M Q3 2014 write-down (~$83M unsold inventory). Production ceased August 2015. Lab126 had layoffs. The retail business absorbed the loss as ~0.2% of annual revenue because Fire Phone was fully ring-fenced in Lab126 with its own budget and leadership (Ian Freed). Bezos (Washington Post, May 2016): "If you think that's a big failure, we're working on much bigger failures right now — and I am not kidding." The 2018 shareholder letter formalized this: "If the size of your failures isn't growing, you're not going to be inventing at a size that can actually move the needle. Amazon will be experimenting at the right scale for a company of our size if we occasionally have multibillion-dollar failures." [25]

Bezos quotes that crystallize the philosophy (verified to shareholder letters by year):

- 1997 founding letter: "We will make bold rather than timid investment decisions where we see a sufficient probability of gaining market leadership advantages. Some of these investments will pay off, others will not, and we will have learned another valuable lesson in either case." [26][27]

- 2011 shareholder meeting (via GeekWire): "Any time you do something big, that's disruptive — Kindle, AWS — there will be critics… you have to be willing to ignore both types of critics." And: "We are stubborn on vision. We are flexible on details." [28]

- 2015 letter (released April 2016): "I believe we are the best place in the world to fail (we have plenty of practice!), and failure and invention are inseparable twins. To invent you have to experiment, and if you know in advance that it's going to work, it's not an experiment." [29]

- 2016 letter (Day 2): "Day 2 is stasis. Followed by irrelevance. Followed by excruciating, painful decline. Followed by death." [30]

Operating mechanisms: 500 annual S-Team goals (each owned by a specific STL with reporting cadence), the PR/FAQ "Working Backwards" process (every product begins with a fictional press release + ≤5-page FAQ before any code is written), six-page narrative memos (PowerPoint banned at S-Team meetings by Bezos email June 9, 2004), and the Bar Raiser hiring process (created 1999, gives a cross-org veto on every hire). Failed bets — Auctions, zShops, WebPay, Local, Destinations, MyHabit, Spark, Dash Buttons, Crucible ($60-80M, May-Nov 2020), Haven (2018-21), Amazon Care (2019-22) — each had its own STL, P&L line, and brand, so shutdowns were surgical. [31]

6. Failure patterns: when the core consumes the bet

Kodak invented the digital camera in December 1975 (Steve Sasson, 0.01 MP, 3.6 kg, 23-second cassette write). Sasson: "The reaction I got from Kodak management was one of curiosity and skepticism… As the company's entire business model was focused around sensitized goods, proposing that they not use any of that was not popular." Marketing told him they "could sell the camera but they wouldn't" — they feared cannibalizing film. Kodak continued digital R&D (1986: 1.4 MP CCD record) but never structurally separated it. Instead the executive team diversified into pharma via the Sterling Drug acquisition ($5.1B, 1988, unwound by 1994). Chapter 11 January 2012. [32]

Blockbuster is the cleanest case of structural protection that worked, then was dismantled. Antioco launched Blockbuster Online + Total Access in 2004, eliminated late fees (~$800M of profit), invested ~$400M. By Q4 2006, Blockbuster Online was growing subscribers faster than Netflix. Then activist Carl Icahn (largest shareholder) and the board concluded the digital investment was destroying near-term profits, ousted Antioco in 2007, installed Jim Keyes, reinstated late fees, defunded digital. Antioco (HBR): "I firmly believe that if our online strategy had not been essentially abandoned, Blockbuster Online would have 10 million subscribers today, and we'd be rivaling Netflix." Bankruptcy September 2010. The structural mechanism that failed was CEO tenure and board alignment — every other piece had been built correctly. [33][34]

Xerox PARC is the opposite failure: invention was structurally protected (Palo Alto, 1970, deliberately isolated), but commercialization was not. PARC invented bitmap GUI, mouse, Ethernet, laser printing, Smalltalk; the Xerox Alto (1973) was the first GUI PC. The Xerox Star 8010 (1981) was a commercial flop at $16,000/workstation. PARC researchers had no incentive to engage Scientific Data Systems (the commercial arm). The copier business had veto power on capex. There was no graduation/reintegration mechanism. Lesson: isolation is necessary but not sufficient. [35]

Nokia lost smartphone share from 49.4% (2007) to 3% (2013) not because they didn't see touchscreens coming — they had prototypes by 2004 — but because of internal fiefdoms (Symbian, S40, Maemo, MeeGo) all competing for resources. Multiple parallel bets = no bet. Stephen Elop's February 2011 "burning platform" memo: "We poured gasoline on our own burning platform… We haven't been delivering innovation fast enough. We're not collaborating internally." Qualcomm's CEO on Nokia: "By the time it made a decision, the opportunity often just went away." Microsoft bought the handset business for €5.44B in September 2013 and wrote off most of it within two years ($7.6B impairment, July 2015 SEC 8-K). [36]

GE Digital / Predix demonstrates that even with separation, sponsorship, and >$4B over six years, a bet fails if (a) the capability is wrong (Predix tried to be horizontal cloud and industrial vertical simultaneously), and (b) the core is forced to consume the bet — inverting the protection logic. Immelt promised $15B in GE Digital revenue by 2020; 2017 reality was ~$4B total digital sales with only ~$500M from Predix. Immelt was retired June 2017; Flannery reset the target to $12B and missed; Larry Culp dismantled the unit from late 2018. The Beth Comstock / Eric Ries FastWorks lean-startup program (5,000 senior managers trained in 4 months) was dismantled with Immelt's exit. Steve Blank: "GE Fastworks wasn't the problem at GE… But the impact of future innovations couldn't compensate for poor execution in its traditional businesses." [37]

Sears Holdings under Lampert (2005-2018) ran a textbook "innovation theater" version: Shop Your Way loyalty + e-commerce was rhetorically the centerpiece (69% of Sears Full-line and Kmart sales in 2013), but operationally Lampert forced internal business units to compete against each other (apparel vs. appliances bidding for marketing) — imposing market discipline on a struggling core rather than structural protection on a bet. Chapter 11 October 2018. [38][39]

Microsoft's pre-Nadella graveyard: Kin (2010, ~$1B over 2 years, pulled within 48 days), Zune ($289M Q1 2007 operating loss, $240M write-down 2008, discontinued 2011 with another ~$290M charge), aQuantive ($6.3B acquisition 2007, $6.2B impairment July 2012 per SEC 8-K), Nokia ($7.2B in 2014, $7.6B impairment + $750-850M restructuring July 2015 per SEC 8-K). These bets had insufficient separation from Windows-centric resource allocation. [40]

7. Healthtech-specific evidence

Teladoc + Livongo ($18.5B all-stock+cash, closed October 2020) is the cautionary tale closest to the Numan situation. Touted as "one app for primary care, chronic care and other virtual care services." Goodwill impairments: $6.6B Q1 2022 (record $6.7B Q1 net loss, -$41.58 EPS), another $3B Q2 2022. Full year 2022: $13.4B non-cash goodwill impairment; $13.7B net loss on $2.4B revenue. CFO Mala Murthy attributed it to "sustained decline in share price… and decreased market multiple for a relevant peer group of high-growth digital healthcare companies." Structural critique: Livongo's chronic-care product was forced into Teladoc's primary-care/televisit organization, killing product velocity; BetterHelp had its own GM but was starved as the core struggled. Gorevic stepped down April 2024. An acquired future bet cannot survive being absorbed into a core that itself is under earnings pressure. [41]

Babylon Health is the UK reference failure. Founded 2013 by Ali Parsa; SPAC at $4.2B October 2021; collapsed by August 2023 (UK Chapter 7 analogue; UK business sold to eMed for £500,000). The fatal flaw was unit economics, not structure: the NHS paid a fixed ~£100/patient/year, but GP-at-Hand patients used the service 6-7 times/year vs. NHS-expected 2-3. Parsa, May 2022: "In reality, people use us six or seven times a year and we lose money on every member that comes in." Royal Wolverhampton NHS 10-year deal terminated after 2 years (5,000 of 300,000 residents signed up). Lesson: structural separation can't fix unit-economic flaws. Fix the economics first. Babylon also illustrates the "trying to be everything" failure: platform + clinical operator + AI vendor + US payer-facing business simultaneously, none separated. [42]

23andMe is the most counter-intuitive lesson. The therapeutics division (established 2015, Richard Scheller as CSO; $300M GSK partnership in 2018) was structurally separate from the consumer business — but the consumer business that funded it was allowed to decline because management attention was on therapeutics. Therapeutics division wholly shut down November 2024 (~200 layoffs, never produced an approved drug). All 7 independent directors resigned in unison September 2024 over Wojcicki's take-private proposal. Chapter 11 March 24, 2025; TTAM Research Institute bought nearly all assets for $305M June 2025. Ex-leader (Fortune): "The company could have been the Google of digital health and it completely whiffed on that." The structural lesson: protecting the bet ≠ protecting the core that funds the bet. Both need protection. [43]

Hims & Hers and Ro illustrate the opposite strategic choice — explicitly not structurally separating new bets. Hims's specialty model (Sexual Health, Mental Health, Dermatology, Weight Loss) operates as a unified platform with each specialty held to a leading indicator ("at least $100M revenue per specialty in 2025" per Q2 2024 shareholder letter). Weight loss launched late 2023; compounded GLP-1 added May 2024 at $199/month (vs. branded $1,000+); projected $725M in 2025. The cost of unified-platform strategy is now visible (May 2026): FDA removing compounded semaglutide from shortage list, SEC investigation into disclosures on compounded GLP-1s, Novo Nordisk lawsuit — and the regulatory exposure on GLP-1 affects the whole company's perception. ARPU slipped $85 → $80. Ro's analogous strategy: vertically integrated pharmacy + manufacturer-direct partnerships (LillyDirect December 2024, NovoCare 2025), which create a de facto structural moat at the channel layer rather than the org-chart layer. [44]

Pharma's structural protection is brand-and-indication, not org-chart. Eli Lilly runs tirzepatide under two brands: Mounjaro (T2D, approved May 2022) and Zepbound (obesity, approved November 8, 2023). Same molecule, two NDAs, two sales forces (endocrinology vs. obesity-medicine), distinct formulary placement, distinct marketing channels. Q1 2025 Lilly revenue $12.73B, +45% YoY. Novo Nordisk runs semaglutide as Ozempic (T2D injectable), Rybelsus (T2D oral), Wegovy (obesity injectable + oral pill, FDA-approved Dec 2025); combined Ozempic + Wegovy ~$26B in 2024. Pharma routinely runs the same molecule under different brands for different indications because customer journey, payer logic, and clinical workflow demand separation. Novo had also been investing in obesity for 20+ years through repeated modest failures (Saxenda/liraglutide) before Wegovy hit — a multi-decade structural commitment. [45]

8. Practical mechanisms (synthesized across cases)

Drawing across 20+ cases, the mechanisms that separate winners from losers are remarkably consistent:

| Mechanism | Worked in | Failed when missing in |

|---|

| Direct reporting to CEO/board (bypassing core P&L) | Apple Project Purple, IBM EBO, Microsoft Azure (Ozzie → Muglia → Nadella) | Kodak digital, Nokia |

| Ring-fenced budget protected from quarterly reallocation | IBM EBO, John Deere ISG, Adobe (CEO-protected revenue trough), AWS pre-2015 | Blockbuster (Total Access defunded), GE Digital post-Immelt |

| Leading-indicator metrics, not revenue/profit | Adobe (ARR), IBM EBO (milestones), Project Purple (ship date) | Sears (store comps), Teladoc (revenue-driven integration) |

| Separate physical/organizational space | Apple "Purple Dorm", IBM PC Boca Raton, Lab126 Palo Alto, Blue River Sunnyvale, AWS Cape Town | Kodak (digital inside film R&D), Nokia (fiefdoms in same buildings) |

| Separate hiring criteria | Apple Purple, IBM EBO (Harreld: small teams, no empire-building), Amazon Bar Raiser | Sears, 23andMe (couldn't pay biotech market rates) |

| CEO-level air cover sustained for years | Jobs (Purple, reportedly ~40% time),Peter FiskDialogue ReviewNarayen (Adobe trough), Nadella (Azure), Palmisano (IBM EBO), Bezos (AWS pre-2015) | Blockbuster (Antioco ousted), GE (Immelt → Flannery), 23andMe |

| Graduation criteria for reintegration | IBM EBO (4 explicit criteria) | Xerox PARC (no reintegration logic), GE Predix (forced reintegration too early) |

| Brand/indication separation while sharing capability | Lilly (Mounjaro/Zepbound), Novo (Ozempic/Wegovy), Deere (acquired subsidiaries) | Teladoc (forced unification of Livongo) |

Adobe deserves special attention as a counter-pattern: most of Creative Cloud was Transformation A (repositioning the core, not building a separate unit). What worked there was not org-chart separation but (a) CEO conviction to hold the line on a guaranteed multi-year revenue trough (FY13 revenue fell ~8%), (b) new leading indicators (ARR) introduced before the trough so Wall Street had something to grade, (c) the narrative was owned at board/IR level. CFO Mark Garrett's message to analysts: don't look at the declining P&L; look at new subscribers and ARR. Trajectory: 1M subscribers Q3 2013 → 3.4M end-2014 → 22M+ by 2019 → $23.77B revenue FY2025. [46]

9. Counter-arguments and when separation goes wrong

Three failure modes for structural separation are well-documented:

"Innovation island" syndrome (Oltra et al., 2022; Oliver, 2019). Skunkworks teams develop identity in opposition to the parent. The team can't transmit knowledge back at reintegration because the core rejects them as foreign or resents their preferential treatment. PSA Peugeot Citroën's Hybrid Air won awards as a prototype, never reached market because the team couldn't reintegrate. Historical AT&T 1980s skunkworks and American Express failures cited in the literature. [47]

Customer-interface separation (Netflix Qwikster, September-October 2011). Hastings split DVD and streaming into separate brands, separate websites, separate billing — internally correct, externally catastrophic. Netflix lost ~800K-1M subscribers in one quarter; stock fell from $304 (July 2011) to <$70 (September 2011), about 75%. Qwikster was killed before launch on October 10, 2011. Hastings: "In hindsight, I slid into arrogance based upon past success." Internal separation can be right; customer-facing separation can be wrong. Don't split the customer experience to optimize the org chart. [48]

Forced internal consumption (GE Predix, Walmart Store No. 8). When core units are required to use the new bet, the new bet becomes a tax rather than a product. GE Aviation and GE Power were forced to use Predix, inflating revenue with bad-customer dynamics. Walmart Store No. 8 (founded 2017 under Marc Lore after $3.3B Jet.com acquisition) closed January 2024 after ~7 years; Jet.com closed June 2020; ModCloth, Bonobos, Jetblack, Moosejaw, Bare Necessities, ShoeBuy all unwound. [49]

When the core is right to resist. Sometimes the strategic bet is a bad bet. Microsoft Kin, Google Glass, Quibi, and Kodak's Sterling Drug acquisition all illustrate that "resistance from the core" is sometimes signal, not noise. 23andMe's therapeutics bet consumed cash the consumer business correctly produced — louder structural resistance from the consumer side might have saved the company. The defensible discipline is not "every bet must be protected" but "the protection mechanism must be earned by milestones."

Reintegration logic matters more than initial separation. IBM EBO had explicit graduation criteria. Pharma never fully reintegrates at the customer interface; brand/indication separation persists indefinitely. Apple reintegrates quickly once the bet ships (iPhone consumed iPod by 2010). Xerox PARC had no reintegration logic and produced gifts to competitors.

Conclusion: where the evidence converges

The convergent finding across Bower (1970), Bower & Christensen (1995, 1996), Christensen (1997, 2003), Mintzberg & Waters (1985), Baghai/Coley/White (1999), O'Reilly & Tushman (2004, 2016, 2021), Govindarajan & Trimble (2005, 2010), Anthony/Gilbert/Johnson (2017), Moore (2015), Blank (2017-2019), the Innosight longevity series (2016-2021), Bain (2016), and BCG's annual Most Innovative Companies surveys is unambiguous: strategic clarity is necessary but not sufficient; structural protection is sufficient when paired with clarity and is the differentiator empirically. The single strongest quantified evidence remains O'Reilly & Tushman's 35-company study: >90% success rate for ambidextrous designs vs. 0% for unsupported teams. [1].pdf)

Three counter-intuitive points are worth surfacing in the post:

First, the failure mode is rational management, not bad management. Christensen: "Good management itself was the root cause." Strategy decks lose to spreadsheets at every prioritization meeting because spreadsheets correctly favor higher-margin near-term opportunities. Telling middle managers "be more strategic" doesn't work — it requires removing the bet from the spreadsheet entirely. [3]

Second, separation without reintegration logic is just gift-giving to competitors (Xerox PARC). IBM EBO is rigorous because it has explicit graduation criteria. Pharma is rigorous because separation is permanent at the brand/indication layer.

Third, the most subtle failure is protecting the bet at the cost of the core (23andMe). Both need active management; both need leading-indicator metrics; both need explicit funding rules. The default failure is the core eating the bet, but the inverse — the bet starving the core — is also documented and lethal.

For a healthtech-specific reader: pharma's Mounjaro/Zepbound and Ozempic/Wegovy dual-branding is the most directly analogous template for separating an obesity book from a healthspan platform while sharing underlying clinical, data, and operational capability. Teladoc/Livongo and Babylon are the cautionary tales. The IBM EBO graduation criteria — leadership team in place, articulated profit path, early market success, proven customer value proposition — are the most rigorous published reintegration discipline.

- Ntnu — http://www.iot.ntnu.no/innovation/norsi-pims-courses/tushman/O%C3%86Reilly%20&%20Tushman%20(2004

- The Innovation Show + 2 — https://theinnovationshow.io/episode/joseph-l-bower-disruptive-technologies-catching-the-wave/

- Goodreads — https://www.goodreads.com/author/quotes/1792.Clayton_M_Christensen

- A-Z Quotes — https://www.azquotes.com/author/2851-Clayton_Christensen

- Summrize — https://www.summrize.com/books/Innovators-Dilemma-Book-Summary

- Scribd — https://www.scribd.com/document/873056406/The-Innovator-s-Dilemma-PDF

- esipfed — https://wiki.esipfed.org/Organization_Capabilities_and_Team_Structures

- Mikepinkel — https://mikepinkel.com/2018/01/14/book-digest-the-innovators-solution/

- Amazon — https://www.amazon.com/Disruptive-Technologies-Catching-Harvard-Business/dp/B000U3J4U4

- Arete Coach — https://www.aretecoach.io/post/22-inspirational-quotes-on-innovation-and-disruption-by-clayton-m-christensen

- Pbworks + 3 — http://soloway.pbworks.com/f/innovators_dilemma%20chapter%20one.pdf

- Christenseninstitute + 3 — https://www.christenseninstitute.org/theory/disruptive-innovation/

- Crain's Detroit Business + 5 — https://www.crainsdetroit.com/article/20140626/BLOG007/140629880/josh-linkner-is-fuming-at-new-yorker-writer

- Units — https://moodle2.units.it/pluginfile.php/577953/mod_resource/content/1/Oreally_Tushman-2004-The%20Ambidextrous%20Organization.pdf

- Barnes & Noble +2 — https://www.barnesandnoble.com/w/lead-and-disrupt-charles-a-oreilly-iii/1138742109

- LinkedIn +3 + 3 — https://www.linkedin.com/pulse/2018-corporate-longevity-forecast-creative-alasdair-trotter

- Mavim + 2 — https://blog.mavim.com/why-70-of-digital-transformations-fail-insights-and-solutions

- Harvard Business Review + 3 — https://hbr.org/podcast/2017/04/to-reinvent-your-firm-do-two-things-at-the-same-time

- Zenorganisations + 2 — https://zenorganisations.com/zone-to-win/

- Harvard Business Review + 6 — https://hbr.org/2019/10/why-companies-do-innovation-theater-instead-of-actual-innovation

- Speakerpedia + 3 — https://speakerpedia.com/speakers/j-bruce-harreld

- Acquired + 6 — https://www.acquired.fm/episodes/amazon-web-services

- Manas J. Saloi + 2 — https://manassaloi.com/booksummaries/2022/06/24/working-backwards-bryar-carr.html

- Virtasant + 3 — https://www.virtasant.com/ai-today/inside-the-framework-that-helps-ceos-disrupt-their-own-companie

- Harvard D3 + 4 — https://d3.harvard.edu/platform-digit/submission/fire-phone-amazons-170-million-summer-fiasco/

- Amazon — https://www.aboutamazon.com/news/company-news/amazons-original-1997-letter-to-shareholders

- Q4cdn — https://s2.q4cdn.com/299287126/files/doc_financials/annual/2016-Letter-to-Shareholders.pdf

- GeekWire + 2 — https://www.geekwire.com/2011/amazons-bezos-innovation/

- The Bezos Letters — https://thebezosletters.com/failure-has-to-be-an-option/

- Amazon — https://www.aboutamazon.com/news/company-news/2016-letter-to-shareholders

- First Round Review + 2 — https://review.firstround.com/how-to-build-an-invention-machine-6-lessons-that-powered-amazons-success/

- Medium + 3 — https://medium.com/@mert.kty81/how-did-kodak-go-bankrupt-how-a-giant-orchestrated-its-own-fall-db1e65dfc884

- Wikipedia — https://en.wikipedia.org/wiki/John_Antioco

- WhatJobs News — https://www.whatjobs.com/news/blockbuster-refused-netflixs-50-million-buy-out-offer-and-then-went-bust/

- Wikipedia + 3 — https://en.wikipedia.org/wiki/Xerox_Alto

- Stratrix + 5 — https://www.stratrix.com/vault/nokia-smartphone-failure

- Platform9 + 6 — https://platform9.com/blog/what-we-can-learn-from-ge-and-why-digital-transformations-fail/

- sec — https://www.sec.gov/Archives/edgar/data/0001310067/000131006714000004/exhibit991-q42013shcearnin.htm

- Americajr — https://americajr.com/news/2018/10/16/sears-holdings-files-chapter-11-bankruptcy-ceo-eddie-lampert-steps-down/

- Medium + 5 — https://medium.com/techtalkers/microsoft-kin-the-billion-dollar-smartphone-disaster-982043c52f91

- Fierce Healthcare + 7 — https://www.fiercehealthcare.com/health-tech/teladoc-takes-3b-impairment-charge-dragging-down-q2-earnings

- Computing + 6 — https://www.computing.co.uk/news/4121796/babylon-health-future-nhs-goes-administration

- PharmaVoice + 5 — https://www.pharmavoice.com/news/23andme-ceo-anne-wojcicki-pharma-drug-development/698919/

- Fierce Healthcare + 4 — https://www.fiercehealthcare.com/digital-health/hims-hers-expands-weight-loss-program-include-access-glp-1-medications

- Eli Lilly and Company + 2 — https://investor.lilly.com/news-releases/news-release-details/treatment-tirzepatide-adults-pre-diabetes-and-obesity-or

- Stratrix + 4 — https://www.stratrix.com/strategic-forks/adobe-creative-cloud

- SMS + 2 — https://sms.onlinelibrary.wiley.com/doi/abs/10.1002/smj.3034

- Yale + 3 — https://cases.som.yale.edu/netflix-and-qwikster/access

- Digital Commerce 360 + 4 — https://www.digitalcommerce360.com/2024/01/23/walmart-closes-startup-incubator-store-no-8/

Commissioned from our research desk. Subject to final editorial discretion.